Which SAQ Do You Need for PCI DSS and How Does It Improve Your Payment Security Strategy?

Introduction

Every business that accepts credit or debit cards faces a critical responsibility: protecting customer payment data. With billions of card transactions processed globally each year, the stakes have never been higher. A single data breach can devastate a company's reputation, trigger massive fines, and erode customer trust that took years to build.

The Payment Card Industry Data Security Standard (PCI DSS) exists to safeguard cardholder information across all payment environments. But here's the challenge: not every business processes payments the same way. A small boutique using a simple card terminal operates very differently from a major online retailer handling thousands of daily transactions. Should they both face identical compliance requirements?

This is where the Self-Assessment Questionnaire (SAQ) transforms the compliance landscape. Instead of forcing every merchant through the same exhaustive validation process, the SAQ offers a flexible, risk-appropriate approach. It recognizes that your compliance path should reflect how you actually handle payment data.

For many businesses, especially small to medium-sized merchants, the SAQ provides a streamlined way to demonstrate PCI DSS compliance without the expense and complexity of full onsite assessments. Yet despite its importance, the SAQ remains widely misunderstood. Many merchants struggle to identify which questionnaire applies to them, how to complete it accurately, or what it truly means for their security posture.

This guide cuts through the confusion. You'll discover exactly what SAQs are, who can use them, how to choose the right type, and the proven steps for successful completion.

What is SAQ?

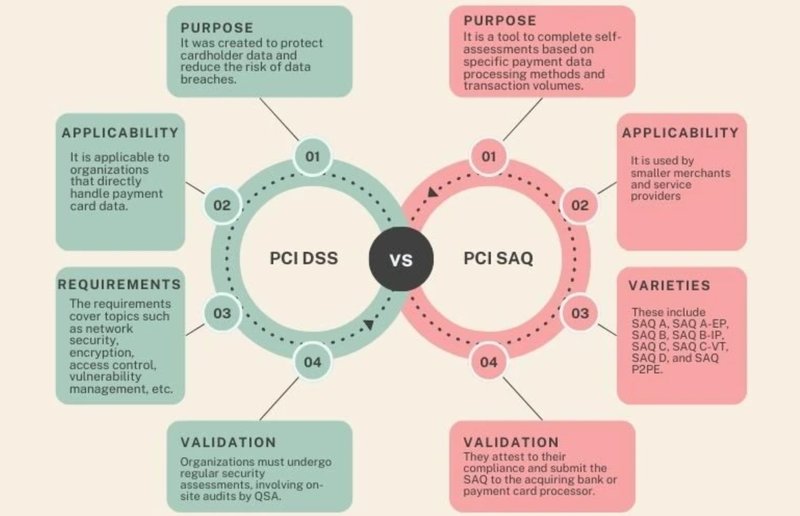

A Self-Assessment Questionnaire (SAQ) is a validation tool designed by the Payment Card Industry Security Standards Council (PCI SSC) to help merchants and service providers assess their compliance with PCI DSS requirements. Think of it as a structured checklist that guides organizations through the security controls relevant to their specific payment processing environment.

Unlike full PCI DSS assessments conducted by Qualified Security Assessors (QSAs), SAQs allow eligible merchants to self-evaluate their compliance status. This approach recognizes that a small coffee shop accepting occasional card payments faces vastly different security challenges than a major e-commerce platform processing thousands of transactions hourly.

The SAQ framework consists of a series of yes-or-no questions covering various security requirements, from network configuration and access controls to encryption standards and monitoring procedures. Each question relates directly to specific PCI DSS requirements, but the number and complexity of questions vary significantly depending on which SAQ type applies to your business.

When you complete an SAQ, you're essentially documenting how your organization meets the security standards appropriate for your payment processing methods. This documentation becomes crucial evidence of your compliance efforts and helps identify any security gaps that need addressing. The process requires honesty and thoroughness, cutting corners or providing inaccurate responses defeats the purpose and leaves your organization vulnerable to both security breaches and potential penalties.

Beyond serving as a compliance tool, SAQs also function as educational resources. Working through the questionnaire helps businesses understand the security landscape better, recognize potential vulnerabilities, and implement stronger protective measures even beyond the minimum requirements.

Who Can Complete an SAQ?

Not every merchant qualifies to use the SAQ approach for PCI DSS validation. Eligibility depends on several factors, including transaction volume, processing methods, and the level of risk associated with your payment environment.

Generally speaking, SAQs are available to merchants who fall into lower risk categories based on how they handle cardholder data. The payment card brands (Visa, Mastercard, American Express, Discover, and JCB) each have their own merchant level classifications, typically determined by annual transaction volume. Smaller merchants, often those processing fewer than six million transactions annually, usually qualify for SAQ-based validation rather than requiring an onsite assessment by a QSA.

However, transaction volume alone doesn't determine SAQ eligibility. The payment channels you use matter significantly. Merchants exclusively using payment terminals that encrypt data before it reaches their systems may qualify for simpler SAQs, while those storing, processing, or transmitting cardholder data in other ways might need more comprehensive questionnaires or even full assessments.

Service providers who handle payment processing on behalf of other businesses may also use SAQs, though they often face stricter requirements than merchants. If your company provides payment gateway services, manages point-of-sale systems for other businesses, or offers similar services, you'll need to carefully determine which validation method applies to your situation.

It's important to note that your acquiring bank (the financial institution processing your card payments) has the final say on whether you can use an SAQ and which type is appropriate. Some acquirers impose stricter requirements than the minimum standards, particularly for higher-risk merchants or those with previous compliance issues. Always consult with your acquirer to confirm your validation requirements before proceeding with an SAQ.

Businesses that have experienced data breaches or security incidents may lose their SAQ eligibility temporarily or permanently, requiring full onsite assessments instead. This emphasizes why maintaining strong security practices matters beyond just checking compliance boxes.

What Are the Types of PCI SAQ and How Do You Choose the Right One?

The PCI SSC has developed nine distinct SAQ types, each tailored to specific payment processing scenarios. Selecting the correct SAQ is absolutely critical choosing the wrong one can invalidate your compliance efforts entirely and leave you exposed to penalties if a breach occurs.

SAQ A applies to card-not-present merchants who have fully outsourced all cardholder data functions to PCI DSS compliant third-party service providers. This is the shortest SAQ, with approximately 22 questions. If you run an e-commerce site that redirects customers to a payment processor's secure page without your systems ever touching card data, SAQ A might be appropriate. However, you cannot store, process, or transmit any cardholder data on your systems, and all payment pages must be hosted externally.

SAQ A-EP is designed for e-commerce merchants who outsource payment processing but whose websites directly impact the security of the payment transaction. This applies when payment pages are hosted on your website (even if actual processing happens elsewhere) or when your site uses iframes to embed third-party payment forms. With around 181 questions, this SAQ is significantly more comprehensive than SAQ A because your website's security directly affects the payment environment.

SAQ B targets merchants using standalone, dial-out terminals with no connection to other systems or the internet. If you operate a brick-and-mortar store using only imprint machines or standalone point-of-sale terminals that don't store cardholder data electronically, this SAQ with approximately 41 questions may be suitable. The key requirement is that these devices must not be connected to any computer system or network.

SAQ B-IP applies to merchants using standalone, PTS-approved payment terminals with IP connectivity but no other connection to business systems. These terminals often process payments through internet connections but remain isolated from your other technology infrastructure. This questionnaire contains around 82 questions and requires demonstrating that the terminals are properly segmented from other network components.

SAQ C-VT is for merchants who manually enter transaction data into internet-based virtual terminals provided by third-party processors. If your staff types credit card information into a web-based payment form rather than swiping or inserting cards into physical terminals, this SAQ with approximately 73 questions likely applies. You must ensure that no cardholder data is stored after authorization and that the computers used to access these terminals are properly secured.

SAQ C covers merchants with payment application systems connected to the internet but no electronic cardholder data storage. This SAQ, containing around 160 questions, applies to businesses using payment applications on computers or mobile devices that directly process transactions but don't retain card data afterward. Network security becomes particularly important with this type.

SAQ P2PE-HW applies exclusively to merchants using validated point-to-point encryption solutions with hardware payment terminals. These systems encrypt card data at the point of interaction, and the merchant never has access to unencrypted card information. With approximately 32 questions, this is one of the shorter SAQs, reflecting the reduced risk these solutions provide. However, the P2PE solution must be listed on the PCI SSC's approved solutions list.

SAQ D for Merchants is the most comprehensive merchant SAQ, containing around 329 questions that cover nearly all PCI DSS requirements. This applies to merchants who don't fit into any other category, including those who store cardholder data electronically or have complex payment environments. Many larger merchants or those with multiple payment channels end up using SAQ D.

SAQ D for Service Providers is designed for service providers who handle payment processing for other organizations. This questionnaire is similarly comprehensive and requires service providers to demonstrate compliance with requirements applicable to their role in the payment ecosystem.

Choosing the right SAQ requires carefully analyzing your payment processing environment. Start by mapping out exactly how payment data flows through your business—from the moment a customer presents their card to when the transaction is authorized and completed. Document every system, application, device, and person that interacts with payment data. Consider whether you store card data (and if so, why), which third-party services you use, and how your networks are configured.

Many businesses mistakenly select simpler SAQs because they seem easier, but this can create serious compliance and liability issues. When in doubt, consult with a QSA or your payment processor to validate your SAQ selection. Some merchants also choose to implement more stringent security measures specifically to qualify for simpler SAQs, which can reduce both compliance burden and risk.

What Are the Steps Used to Complete an SAQ?

Successfully completing an SAQ involves more than just answering questions. It requires a systematic approach that ensures accurate assessment, proper documentation, and meaningful security improvements.

Step One: Confirm Your SAQ Type

Before diving into questions, absolutely verify you're using the correct SAQ. Review your payment processing methods with your acquiring bank or payment processor. Understand exactly how cardholder data moves through your environment and which systems interact with it. If your business has changed since your last assessment, perhaps you've added an e-commerce channel or switched payment processors, your SAQ type may need to change as well.

Step Two: Understand the Scope

Scoping determines which systems, networks, people, and processes fall under PCI DSS requirements. This includes any system component that stores, processes, or transmits cardholder data, as well as systems connected to these components. Proper scoping is crucial because it defines where you'll need to implement security controls and which areas will be evaluated during your SAQ completion.

Network segmentation can dramatically reduce your scope by isolating payment systems from other business systems. If your payment processing environment is properly segmented and the segmentation is validated, many of your business systems may fall outside PCI scope, simplifying compliance considerably.

Step Three: Gather Documentation and Evidence

Before answering questions, collect the documentation you'll need to support your responses. This might include network diagrams, firewall configurations, access control policies, security awareness training records, vendor management documentation, vulnerability scan results, and penetration testing reports. Having these materials organized beforehand makes the process more efficient and ensures your answers reflect actual practices rather than intentions.

Step Four: Answer Each Question Honestly and Thoroughly

Work through the SAQ methodically, answering every applicable question based on your actual environment and practices. Each question requires a response indicating whether the requirement is in place, not applicable, or includes compensating controls. Don't rush this step, take time to verify that your answers accurately reflect your security posture.

If a requirement isn't fully met, document why and create a remediation plan. Aspirational answers that don't reflect reality provide no real security benefit and can create liability if a breach occurs. Remember that the SAQ is a tool for improving security, not just achieving a checkmark.

Step Five: Address Gaps and Implement Remediation

For any requirements you can't fully meet, develop a clear action plan with specific steps, responsible parties, and target completion dates. Prioritize remediations based on risk, address critical vulnerabilities immediately while scheduling less urgent improvements appropriately. Some gaps might require technology investments, policy updates, training programs, or process changes.

Step Six: Obtain Required Attestations and Scans

Most SAQs require quarterly network vulnerability scans performed by Approved Scanning Vendors (ASVs). These external scans identify security weaknesses in internet-facing systems. Ensure you have passing scan results from the relevant quarters before attesting to compliance. Some SAQ types also require additional documentation like penetration testing results or segmentation validation.

Step Seven: Complete the Attestation of Compliance

Once you've answered all questions and addressed any gaps, complete the Attestation of Compliance (AOC). This document officially declares your compliance status and must be signed by an authorized company executive, acknowledging responsibility for maintaining PCI DSS compliance. The attestation includes details about your assessment, the SAQ type used, and confirmation that requirements are met.

Step Eight: Submit Documentation to Required Parties

Submit your completed SAQ and AOC to your acquiring bank or payment processor according to their requirements. Some may also require supporting documentation. Keep copies of all submitted materials for your records. Most organizations must revalidate compliance annually, so maintaining organized documentation streamlines future assessments.

Step Nine: Maintain Ongoing Compliance

Completing an SAQ is an ongoing commitment. PCI DSS compliance requires continuous attention to security practices, regular monitoring, periodic testing, and prompt responses to new vulnerabilities. Schedule regular reviews of your controls, stay informed about emerging threats, and ensure your team remains trained on security best practices.

Assign someone in your organization responsibility for maintaining PCI compliance throughout the year. This person should monitor security alerts, coordinate vulnerability scans, manage policy updates, and prepare for the next annual assessment. Waiting until just before your next SAQ deadline often results in scrambling to address issues that could have been handled proactively.

FAQs

How often do I need to complete an SAQ?

Most merchants must complete an SAQ annually. However, you should reassess your compliance immediately if you make significant changes to your payment processing environment, such as implementing new payment technologies, changing service providers, or expanding into new sales channels. Additionally, quarterly vulnerability scans are required throughout the year.

What happens if I can't answer "yes" to all SAQ questions?

If you have gaps in compliance, document them clearly and create remediation plans with specific timelines. You may still be able to submit your SAQ with documented action plans, depending on your acquiring bank's requirements. However, you should prioritize addressing compliance gaps quickly, as they represent real security vulnerabilities.

Can I complete an SAQ myself, or do I need outside help?

Eligible merchants can complete SAQs without hiring external assessors. However, many businesses benefit from consulting with PCI DSS experts, particularly when determining SAQ type, scoping their environment, or implementing complex security controls. The investment in expert guidance often pays for itself through more efficient compliance and better security.

What's the difference between a PCI DSS and an SAQ?

PCI DSS is the comprehensive security standard itself, containing twelve high-level requirements and numerous sub-requirements covering all aspects of payment security. The SAQ is a validation tool that helps eligible merchants demonstrate compliance with the PCI DSS requirements relevant to their specific payment environment.

Do I need to be PCI compliant if I only process a few transactions?

Yes. PCI DSS compliance applies to any organization that accepts, transmits, or stores cardholder data, regardless of transaction volume. However, smaller merchants typically qualify for simpler validation methods like SAQ A or B, which are less burdensome than full assessments while still ensuring basic security standards.

What are compensating controls?

Compensating controls are alternative security measures implemented when you cannot meet a specific PCI DSS requirement exactly as stated. To be valid, compensating controls must meet the intent and rigor of the original requirement, provide similar protection, and be above and beyond other PCI requirements. They require careful documentation and may need approval from your acquiring bank.

Will completing an SAQ prevent all payment card fraud?

While SAQ completion significantly reduces security risks, no security measure offers absolute protection. PCI DSS compliance should be viewed as a strong foundation for payment security, but organizations should also implement additional fraud prevention measures, stay informed about emerging threats, and maintain a comprehensive security program beyond minimum compliance requirements.

Conclusion

The Self-Assessment Questionnaire represents a practical, risk-based approach to PCI DSS compliance that acknowledges the diverse nature of modern payment processing. By tailoring validation requirements to specific payment environments, the SAQ framework allows businesses of all sizes to achieve meaningful security without unnecessary complexity.

However, SAQs should never be treated as mere paperwork exercises. They're opportunities to genuinely assess and improve your organization's payment security posture. The questions prompt critical thinking about vulnerabilities, encourage implementation of proven security controls, and help build a culture where protecting customer payment data becomes a fundamental business priority.

As payment technologies evolve and cyber threats become more sophisticated, the role of structured compliance frameworks like PCI DSS and tools like the SAQ becomes increasingly important. Businesses that approach SAQ completion thoughtfully, viewing it as a security enhancement rather than a burden; position themselves to build customer trust, avoid costly breaches, and operate with confidence in an increasingly digital marketplace.

Remember that annual SAQ completion marks important milestones, but genuine payment security requires daily attention, continuous improvement, and unwavering commitment from your entire organization.

Take Control of Your PCI Compliance Journey with Regulance. Contact Regulance today to schedule a consultation and discover how we can simplify your path to PCI DSS compliance while strengthening your overall security posture.