What is PCI DSS Level 3 and Who Does It Apply To?

Introduction

Payment card security has become a critical concern for businesses of all sizes. Every time a customer swipes, taps, or enters their card details, sensitive financial information travels through a complex network of merchants, processors, and payment gateways. This is where the Payment Card Industry Data Security Standard (PCI DSS) comes in, establishing a comprehensive framework to protect cardholder data from theft and fraud.

PCI DSS recognizes that a small boutique processing a few hundred transactions annually faces different security challenges than a major retailer handling millions of payments. To address this reality, PCI DSS has established four distinct compliance levels, each with tailored requirements based on transaction volume. Understanding which level applies to your business is the first step toward securing your payment operations and protecting your customers.

For many growing businesses, PCI DSS Level 3 represents a significant milestone. It signals that your organization has reached a substantial transaction volume and must now demonstrate a more rigorous approach to payment security. But what exactly does Level 3 entail? Who needs to comply? And how does it differ from other compliance levels? This article will answer these questions and provide you with the knowledge you need to navigate PCI DSS Level 3 successfully.

What is PCI DSS Level 3?

PCI DSS Level 3 is the third tier of compliance in the Payment Card Industry Data Security Standard framework, specifically designed for merchants processing between 20,000 and 1 million e-commerce transactions annually across all card brands. This classification targets mid-sized businesses that have grown beyond small-scale operations but haven't yet reached enterprise-level transaction volumes.

The Payment Card Industry Security Standards Council, a collaborative effort between major card brands including Visa, Mastercard, American Express, Discover, and JCB, created this tiered approach to ensure proportionate security measures. Level 3 strikes a balance between the lighter requirements of Level 4 and the intensive scrutiny applied to Level 1 and Level 2 merchants.

PCI DSS Level 3 requires businesses to implement all 12 fundamental requirements of the PCI DSS framework. These requirements encompass building and maintaining secure networks, protecting cardholder data, maintaining vulnerability management programs, implementing strong access control measures, regularly monitoring and testing networks, and maintaining comprehensive information security policies.

What distinguishes Level 3 from lower levels is the validation method. Level 3 merchants must complete an annual Self-Assessment Questionnaire, which is a detailed document requiring businesses to evaluate their compliance with each applicable PCI DSS requirement. Additionally, they must perform quarterly network scans by an Approved Scanning Vendor to identify vulnerabilities in their external-facing systems.

The self-assessment approach recognizes that while Level 3 merchants handle significant transaction volumes, they may not require the expensive on-site assessments mandated for higher levels. However, this doesn't mean compliance is any less important. Level 3 merchants must take their obligations seriously, as they process enough transactions to represent attractive targets for cybercriminals.

It's important to note that individual card brands may have slight variations in their exact definitions and requirements for Level 3. Some card brands focus exclusively on e-commerce transactions, while others may include all card-not-present transactions in their calculations. Businesses should verify their specific classification with their acquiring bank and review requirements for each card brand they accept.

Who Does It Apply To?

PCI DSS Level 3 applies to a specific category of merchants based on their annual transaction volume, but understanding exactly who falls into this classification requires examining several factors beyond just numbers.

Transaction Volume Criteria

The primary criterion for Level 3 classification is processing between 20,000 and 1 million e-commerce transactions per year across all card brands combined. This means if your business processes 15,000 Visa transactions, 10,000 Mastercard transactions, and 5,000 American Express transactions online annually, you would total 30,000 e-commerce transactions and fall into Level 3.

It's crucial to understand that this calculation specifically refers to e-commerce or card-not-present transactions where the customer isn't physically present during the sale. This includes online purchases through your website, telephone orders, mail orders, and recurring billing arrangements. Face-to-face card-present transactions using physical terminals are generally calculated separately under different criteria.

Business Types and Industries

Level 3 compliance typically applies to growing e-commerce businesses, online subscription services, digital product retailers, software-as-a-service companies, online educational platforms, and medium-sized B2B companies that process payments electronically. These businesses have successfully scaled beyond the startup phase but haven't yet reached the massive transaction volumes of major enterprises.

For example, a regional online retailer selling specialty products, a subscription box service with several thousand active customers, a boutique software company offering monthly subscriptions, or a mid-sized consulting firm processing client payments online would all likely fall into Level 3 territory.

Service Providers

Service providers that handle, process, or store cardholder data on behalf of other companies also have compliance obligations. A service provider processing between 20,000 and 1 million transactions annually would be classified as a Level 3 service provider, though their validation requirements may differ slightly from merchant requirements.

Geographic Considerations

PCI DSS applies globally to any organization that accepts payment cards from the major card brands, regardless of where they're located. Whether you're operating in North America, Europe, Asia, Africa, or anywhere else, if you're processing card payments within the specified volume range, Level 3 requirements apply to you.

Acquiring Bank Determinations

Your acquiring bank or payment processor plays a crucial role in determining your PCI DSS level. They track your transaction volumes and inform you of your compliance obligations. Some acquiring banks may impose stricter requirements than the baseline standards, so it's essential to maintain open communication with your payment partners about your compliance status.

Multiple Business Divisions

If your organization operates multiple divisions or brands, transaction volumes are typically aggregated across all entities using the same merchant identification number. However, if different divisions have separate merchant accounts with different acquiring banks, they may be evaluated independently.

What Are the Benefits of PCI DSS Level 3 Compliance?

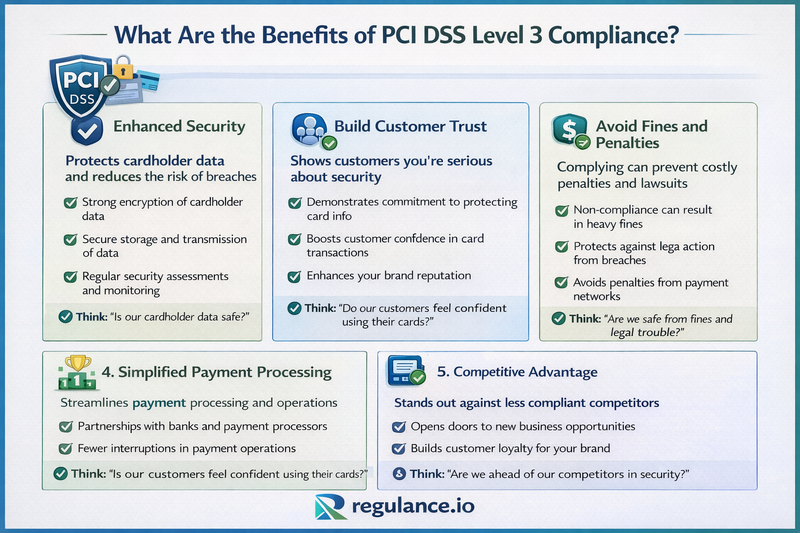

Achieving and maintaining PCI DSS Level 3 compliance delivers substantial advantages that extend far beyond simply meeting regulatory obligations. These benefits impact your security posture, business operations, customer relationships, and bottom line.

Enhanced Data Security and Reduced Breach Risk

PCI DSS Level 3 compliance is significantly improved security for payment card data. By implementing the standard's comprehensive requirements, you create multiple layers of defense against cyber threats. These include firewalls protecting cardholder data environments, encryption of transmitted data, regular security testing, and strict access controls. This multi-faceted approach dramatically reduces your vulnerability to data breaches, which can be devastating both financially and reputationally.

Statistics consistently show that non-compliant merchants experience higher rates of payment card breaches. By investing in Level 3 compliance, you're building a robust security infrastructure that protects your business and your customers from the ever-evolving landscape of cyber threats.

Avoiding Costly Penalties and Fines

Non-compliance with PCI DSS can result in severe financial penalties imposed by card brands and acquiring banks. These fines can range from $5,000 to $100,000 per month until compliance is achieved, depending on the severity of violations and breach history. For Level 3 merchants, these penalties can quickly escalate to amounts that threaten business viability.

Beyond direct fines, non-compliant merchants may face increased transaction fees, forensic investigation costs if a breach occurs, and potential termination of their ability to accept card payments entirely. Maintaining Level 3 compliance helps you avoid these financial pitfalls and ensures uninterrupted payment processing capabilities.

Building Customer Trust and Loyalty

Today's consumers are increasingly aware of data security issues and concerned about protecting their personal information. When customers know you're PCI DSS compliant, it signals that you take their security seriously and have implemented industry-standard protections for their payment data.

This trust translates directly into customer confidence, higher conversion rates, and increased loyalty. Customers are more likely to complete purchases and return for future transactions when they feel their payment information is secure. In contrast, security concerns represent one of the primary reasons for shopping cart abandonment in e-commerce.

Competitive Market Advantage

PCI DSS Level 3 compliance can serve as a powerful differentiator in crowded markets. Being able to demonstrate compliance gives you credibility that competitors lacking certification cannot match. This advantage is particularly valuable when pursuing partnerships, enterprise clients, or customers in regulated industries who require verified security standards from their vendors.

Many B2B customers and partners now require proof of PCI DSS compliance before entering business relationships. By achieving Level 3 compliance proactively, you remove potential barriers to these opportunities and position your business as a trustworthy partner.

Improved Operational Efficiency

The process of achieving PCI DSS compliance often reveals inefficiencies in your payment processing workflows and security procedures. Implementing the standard's requirements typically leads to streamlined processes, better documentation, clearer security protocols, and more efficient incident response capabilities.

These operational improvements reduce the likelihood of errors, speed up troubleshooting when issues occur, and create a more organized approach to managing your payment environment. The result is not just better security but smoother day-to-day operations.

Protection Against Liability

In the unfortunate event of a payment card data breach, demonstrated PCI DSS compliance can significantly reduce your liability exposure. While compliance doesn't eliminate all liability, it shows you took reasonable precautions and followed industry standards, which can influence legal outcomes, insurance claims, and negotiations with affected parties.

Conversely, being non-compliant at the time of a breach dramatically increases your liability and can result in additional penalties beyond those directly related to the breach itself.

Foundation for Business Growth

As your business continues growing, PCI DSS Level 3 compliance provides a solid foundation for scaling your payment operations. The security infrastructure and processes you build for Level 3 will serve you well as transaction volumes increase, making the eventual transition to Level 2 or Level 1 much smoother.

Additionally, compliance demonstrates to investors, lenders, and potential acquirers that your business maintains professional-grade security standards and takes risk management seriously, which can facilitate funding opportunities and improve business valuation.

What Are the Differences Between Level 2 and Level 3?

Understanding the distinctions between PCI DSS Level 2 and Level 3 is essential for businesses approaching these thresholds and planning their compliance strategies. While both levels require adherence to the same 12 core PCI DSS requirements, they differ significantly in transaction volume thresholds, validation methods, and practical implementation approaches.

Transaction Volume Thresholds

The most fundamental difference lies in the transaction volumes that define each level. PCI DSS Level 3 applies to merchants processing between 20,000 and 1 million e-commerce transactions annually, while Level 2 covers merchants processing between 1 million and 6 million total transactions per year across all channels.

This volume difference is significant because it typically reflects a substantial difference in business scale, resources, and risk exposure. Level 2 merchants represent larger operations with more complex payment infrastructures and greater potential impact if a breach occurs.

Validation and Assessment Requirements

The validation process represents the most practical difference between these levels. Level 3 merchants must complete an annual Self-Assessment Questionnaire and undergo quarterly network scans by an Approved Scanning Vendor. This self-attestation approach allows businesses to evaluate their own compliance with guidance but without external audit.

Level 2 merchants, depending on card brand requirements and acquiring bank policies, may be required to complete either an annual Self-Assessment Questionnaire or undergo an annual on-site assessment by a Qualified Security Assessor. Many acquiring banks require Level 2 merchants to have external QSA validation rather than self-assessment, representing a significant increase in both scrutiny and cost.

The QSA assessment involves external security professionals conducting thorough on-site evaluations of your payment card environment, interviewing personnel, reviewing documentation, testing security controls, and validating that all PCI DSS requirements are properly implemented. This process is considerably more intensive, time-consuming, and expensive than self-assessment.

Cost Implications

The financial investment required for compliance differs substantially between levels. Level 3 merchants can typically achieve compliance with relatively modest budgets, primarily covering the cost of quarterly external vulnerability scans, security tools and technologies, possible consulting support for self-assessment completion, and internal staff time.

Level 2 merchants face significantly higher costs if required to undergo QSA assessments, which can range from $15,000 to $50,000 or more annually depending on the complexity of the payment environment. These costs come in addition to the ongoing expenses of maintaining security controls and conducting quarterly scans.

Documentation and Evidence Requirements

While both levels require comprehensive documentation, Level 2 merchants undergoing QSA assessments face more rigorous evidence requirements. They must provide detailed documentation of policies, procedures, system configurations, security testing results, and operational practices to external assessors who will verify everything thoroughly.

Level 3 merchants completing self-assessments still need solid documentation, but the evidence review process is internal rather than external. This distinction means Level 2 organizations typically need more formalized documentation practices and evidence-gathering procedures.

Risk Profile and Scrutiny

Card brands and acquiring banks view Level 2 merchants as presenting higher risk due to their larger transaction volumes. This perception often results in increased scrutiny, more frequent compliance verification, stricter contractual requirements, and potentially higher penalties for non-compliance.

Level 3 merchants, while still important, generally face less intensive oversight and may have more flexibility in how they approach certain security requirements, particularly in areas where multiple implementation options exist.

Attestation of Compliance

Both levels must submit an Attestation of Compliance to their acquiring bank, but the weight of this attestation differs. For Level 3, it represents internal verification of compliance. For Level 2 merchants with QSA assessments, it comes with external validation from security professionals, providing stronger assurance to card brands and acquiring banks.

Transitional Considerations

As Level 3 merchants approach the 1 million transaction threshold, they should begin preparing for potential Level 2 requirements. This transition planning should include budgeting for potential QSA assessments, enhancing documentation practices, implementing more formal security processes, and conducting gap analyses against external assessment standards.

Understanding these differences helps businesses anticipate compliance costs, plan security investments appropriately, and ensure they're meeting the right requirements for their transaction volume level.

How Regulance Helps You Achieve PCI DSS Compliance

Regulance transforms the complex compliance journey into a straightforward, manageable process that actually makes sense for your business.

Guided Compliance Made Simple

Regulance walks you through every PCI DSS requirement with intelligent, step-by-step workflows tailored to your specific business model. No more drowning in confusing technical jargon or wondering if you've missed something critical. The platform adapts to how you process payments, showing you only what's relevant to your situation and cutting out unnecessary complexity.

Automated Assessments That Save Time

Instead of struggling through lengthy Self-Assessment Questionnaires alone, Regulance guides you with smart questionnaires that understand your payment environment. The platform automatically collects evidence, tracks your progress, and highlights exactly what needs attention, turning weeks of manual work into days of focused action.

Always-On Compliance Monitoring

The platform continuously monitors your security posture with real-time dashboards showing your compliance status at a glance. Automated alerts notify you of issues before they become problems, while integrated vulnerability scanning keeps you ahead of emerging threats.

Expert Support When You Need It

You're not alone in this. Regulance connects you with PCI DSS specialists who provide clear answers to your questions, review your implementations, and guide you through complex requirements. It's like having a compliance team without the overhead of hiring one.

Strategic Roadmap to Compliance

Gap analysis tools identify security shortfalls, prioritize fixes based on actual risk, and create actionable roadmaps that fit your budget and timeline. You'll know exactly what to do next and why it matters.

Cost-Effective Compliance

For a fraction of the cost of hiring consultants or full-time compliance staff, Regulance delivers enterprise-grade compliance management. The platform pays for itself by reducing the time, confusion, and resources typically required for PCI DSS compliance giving you back hours to focus on growing your business.

Frequently Asked Questions

How often do Level 3 merchants need to validate PCI DSS compliance?

Level 3 merchants must complete their Self-Assessment Questionnaire annually and undergo quarterly network vulnerability scans by an Approved Scanning Vendor. Additionally, you should continuously monitor your compliance status and update your attestation whenever significant changes occur in your payment card environment.

What happens if my business moves from Level 4 to Level 3?

When your transaction volume grows from Level 4 to Level 3, your compliance obligations become more formal. You'll need to complete a full Self-Assessment Questionnaire rather than the potentially simplified version available at Level 4, begin quarterly external vulnerability scanning, and submit an Attestation of Compliance to your acquiring bank. Most businesses should begin preparing for these requirements several months before crossing the 20,000 transaction threshold.

Can I complete the PCI DSS Level 3 Self-Assessment Questionnaire myself?

Yes, Level 3 merchants can complete their SAQ internally without hiring external assessors. However, having at least some compliance expertise is highly recommended, whether through internal staff training, compliance platform guidance like Regulance, or consultation with PCI DSS specialists. The SAQ is detailed and technical, and mistakes can leave you non-compliant despite believing otherwise.

How much does PCI DSS Level 3 compliance typically cost?

Costs vary widely based on your current security posture, technical infrastructure, and chosen approach. Typical costs include $2,000-5,000 for quarterly external scans annually, $5,000-15,000 for security tools and technologies, $3,000-10,000 for compliance platform subscriptions or consulting support, and internal staff time. Total first-year costs typically range from $10,000 to $30,000, with lower ongoing maintenance costs in subsequent years.

What is the difference between the various SAQ types?

PCI DSS offers different SAQ types based on how you process payments. SAQ A is for e-commerce merchants who outsource all payment processing, SAQ A-EP is for e-commerce merchants with direct connections to payment processors, SAQ D is the comprehensive version for merchants not meeting criteria for other types, and several other specialized versions exist. Your acquiring bank or compliance platform can help determine which SAQ type applies to your business model.

Do I need to be PCI DSS compliant if I use a third-party payment processor?

Yes, even when using third-party payment processors like Stripe, Square, or PayPal, you still have PCI DSS compliance obligations, though they may be significantly reduced. The key is ensuring cardholder data never touches your systems by using hosted payment pages, tokenization, or point-to-point encryption. This approach can qualify you for simpler SAQ types with fewer requirements, but you're never completely exempt from PCI DSS.

What are the consequences of failing a PCI DSS compliance audit?

For Level 3 merchants using self-assessment, there isn't a formal "fail" since you're not being externally audited. However, if your acquiring bank determines you're non-compliant, consequences can include monthly non-compliance fees ranging from $5,000 to $25,000, increased transaction processing fees, mandatory compliance timelines with monitoring, and potentially losing the ability to accept card payments if non-compliance persists.

How long does it typically take to achieve PCI DSS Level 3 compliance?

Timeline varies based on your starting point, but most businesses require 3-6 months for their initial compliance project. This includes security assessment and gap analysis, implementing required controls and security measures, policy development and documentation, completing the SAQ, and passing initial vulnerability scans. Organizations starting with strong security foundations may achieve compliance faster, while those requiring significant infrastructure changes may need longer.

Does PCI DSS Level 3 compliance guarantee I won't experience a data breach?

No compliance framework can guarantee complete protection against breaches, as the threat landscape constantly evolves and determined attackers have sophisticated capabilities. However, PCI DSS compliance significantly reduces your risk by implementing proven security controls, establishing monitoring and response capabilities, and creating security-aware organizational cultures. Most breaches occur at non-compliant organizations or those with lapses in maintaining their security controls.

Can I lose my Level 3 status and move to a higher level?

Yes, if your transaction volumes increase beyond 1 million e-commerce transactions annually, you'll move to Level 2, which has more stringent validation requirements. Conversely, if volumes decrease below 20,000 transactions, you may move to Level 4. Your acquiring bank monitors your transaction volumes and will notify you of changes in your compliance level, though you should also track this internally to prepare appropriately.

Conclusion

PCI DSS Level 3 represents a critical milestone for growing businesses in the digital economy. As your organization processes between 20,000 and 1 million e-commerce transactions annually, you've achieved a level of success that comes with increased responsibility for protecting customer payment data. Understanding and embracing these compliance requirements isn't just about avoiding penalties; it's about building the security foundation your business needs to continue growing safely and sustainably.

The journey to PCI DSS Level 3 compliance may seem daunting initially, particularly when you're managing numerous other business priorities. However, the benefits far outweigh the challenges. Enhanced security protects your business from the devastating financial and reputational damage of data breaches. Compliance opens doors to partnerships and customers who require verified security standards. The operational improvements you'll implement create efficiencies that benefit your organization beyond payment security. Most importantly, you'll build trust with customers who increasingly value businesses that take their data protection seriously.

The key to successful compliance lies in approaching it systematically rather than as a last-minute scramble. Start by accurately determining your compliance level based on transaction volumes across all card brands. Understand which Self-Assessment Questionnaire type applies to your payment processing model. Conduct an honest assessment of your current security posture and identify gaps. Then develop a realistic implementation plan that addresses requirements methodically while maintaining your business operations.

Leveraging specialized compliance platforms like Regulance can dramatically simplify this journey by providing structure, automation, and expertise that many mid-sized businesses lack internally. These tools transform compliance from an overwhelming checklist into a manageable process with clear steps and measurable progress.

As your business continues growing, the compliance infrastructure you build today will serve as a foundation for tomorrow's success. Whether you remain at Level 3 or eventually transition to Level 2 or even Level 1, the security practices, documentation systems, and compliance mindset you develop now will scale with your organization.

Start your compliance journey with Regulance today, and transform payment card security from a regulatory burden into a competitive advantage that drives your business forward.