Understanding PCI DSS Compliance Levels 1-4: A Comprehensive Guide for Businesses

Introduction

Every time a customer swipes their credit card at your business, you're handling data worth its weight in digital gold and with that privilege comes the responsibility of protecting it. The Payment Card Industry Data Security Standard (PCI DSS) isn't just another compliance checkbox; it's your shield against the $4.35 million average cost of a data breach that could devastate your business overnight. Whether you process 20,000 transactions annually or 6 million, understanding which of the four PCI DSS compliance levels applies to your business determines everything from your validation requirements to your audit obligations—and getting it wrong could mean the difference between seamless operations and regulatory nightmares that keep you awake at night.

The Four PCI DSS Compliance Levels Explained

PCI DSS compliance is divided into four levels, depending on the annual amount of a business process credit or debit card transactions. Each level has distinct requirements, validation methods, and compliance obligations that scale with the volume of transactions processed.

Level 1: The Highest Risk Category

Transaction Volume: Over 6 million card transactions annually (any brand) or over 2.5 million Visa transactions annually

Who Qualifies: Large retailers, major e-commerce platforms, payment processors, and global corporations

Requirements:

- Annual on-site security assessment by a Qualified Security Assessor (QSA)

- Quarterly network vulnerability scanning by an Approved Scanning Vendor (ASV)

- Annual Report on Compliance (ROC)

- Attestation of Compliance (AOC)

- Comprehensive penetration testing

Level 1 merchants face the most stringent requirements due to the massive volume of sensitive data they handle. The annual on-site assessment involves a thorough examination of all security controls, policies, and procedures. These organizations must also maintain detailed documentation of their security infrastructure and undergo regular testing of their defenses.

Level 2: High-Volume Processing

Transaction Volume: 1 million to 6 million card transactions annually (any brand) or 300,000 to 2.5 million Visa transactions annually

Who Qualifies: Mid-sized retailers, regional chains, growing e-commerce businesses

Requirements:

- Annual Self-Assessment Questionnaire (SAQ) or on-site assessment

- Quarterly vulnerability scanning by ASV

- Annual AOC

- May require penetration testing depending on the payment environment

Level 2 merchants have more flexibility in their validation approach. If you're a Level 2 or Level 3 merchant, you may have opportunities to lighten or streamline your PCI DSS compliance requirements. Many Level 2 merchants can complete SAQ D, which covers 252 requirements, but those using certain payment solutions may qualify for SAQ A-EP, reducing requirements to 151.

Level 3: Mid-Range Processors

Transaction Volume: 20,000 to 1 million e-commerce transactions annually (any brand) or 20,000 to 300,000 Visa transactions annually

Who Qualifies: Small to medium-sized online businesses, local chains with significant card processing

Requirements:

- Annual Self-Assessment Questionnaire (SAQ)

- Quarterly vulnerability scanning by ASV (if storing cardholder data)

- Annual AOC

- Network segmentation validation may be required

Level 3 merchants typically complete one of several SAQ variants based on their payment processing methods. The specific SAQ type depends on how the business handles cardholder data, with options ranging from SAQ A (for outsourced payment processing) to SAQ D (for comprehensive in-house processing).

Level 4: Lowest Volume Category

Transaction Volume: Fewer than 20,000 e-commerce transactions annually (any brand) or fewer than 20,000 Visa transactions annually (including other card brands)

Who Qualifies: Small businesses, local merchants, service providers with minimal card processing

Requirements:

- Annual Self-Assessment Questionnaire (SAQ)

- Annual AOC

- Quarterly vulnerability scanning (only if storing cardholder data)

Level 4 represents the majority of merchants worldwide. These businesses typically use simpler SAQ forms, with many qualifying for SAQ A if they outsource all payment processing to PCI-compliant service providers. However, even Level 4 merchants must maintain security awareness and implement basic protection measures.

Key Compliance Requirements Across All Levels

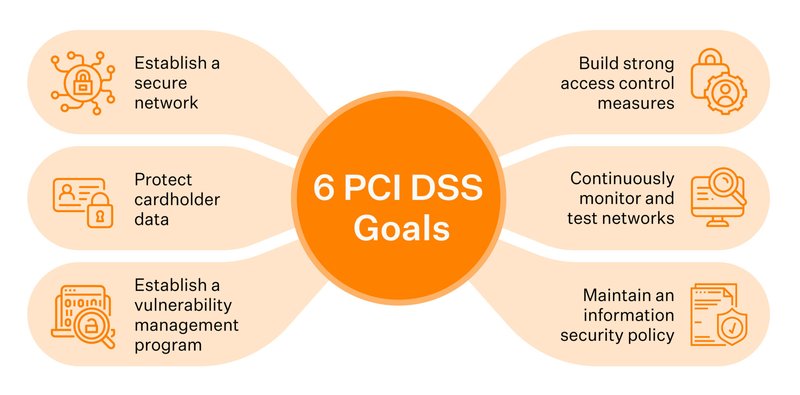

Regardless of their compliance level, all merchants must adhere to PCI DSS's 12 core requirements, organized into six control objectives:

Build and Maintain a Secure Network

Install and maintain firewall configurations

Avoid using vendor-supplied defaults for passwords and security parameters

Protect Cardholder Data

Protect stored cardholder data

Encrypt transmission of cardholder data across open networks

Maintain a Vulnerability Management Program

Protect systems against malware.

Develop and maintain secure systems and applications.

Implement Strong Access Control Measures

Restrict access to cardholder data on a business need-to-know basis.

Identify and authenticate access to system components.

Restrict physical access to cardholder data

Regularly Monitor and Test Networks

Track and monitor all access to network resources and cardholder data

Regularly test security systems and processes

Maintain an Information Security Policy

Maintain a policy that addresses information security for all personnel

Important 2025 Compliance Updates

Starting March 31st, 2025, PCI DSS requirements 6.4.3 and 11.6.1 will go from being best practices to mandatory. These requirements focus on:

- Requirement 6.4.3: Public-facing web applications must be protected against attacks

- Requirement 11.6.1: Security testing procedures must be implemented and maintained

Businesses collecting payments online via webpages need to ensure their systems meet these mandatory requirements by the March deadline to maintain compliance.

The Financial Impact of Non-Compliance

The cost of non-compliance far exceeds the investment in proper security measures. PCI compliance fines can vary from $5,000 to $100,000 a month depending on the size of the company and the duration and scope of non-compliance.

Beyond fines, businesses face additional consequences including:

Direct Financial Costs:

- Monthly penalty fees from card brands

- Increased transaction processing fees

- Forensic investigation costs

- Card reissuance fees

- Legal expenses from potential lawsuits

Business Impact:

- Loss of ability to process credit cards

- Reputation damage and customer loss

- Increased insurance premiums

- Regulatory scrutiny and additional audits

Breach-Related Expenses: PCI DSS compliance protects against data breaches and cyber threats, ensuring a secure and trustworthy operation. When breaches occur, costs escalate dramatically through notification expenses, credit monitoring services, and long-term customer acquisition challenges.

Compliance Costs by Level

Understanding the financial investment required for each compliance level helps businesses budget appropriately:

Level 1 Compliance Costs:

- QSA assessment: $25,000 - $75,000 annually

- Vulnerability scanning: $3,000 - $10,000 annually

- Penetration testing: $15,000 - $50,000 annually

- Internal security team or consultants: $100,000+ annually

Level 2-3 Compliance Costs:

- SAQ completion (with consultant): $5,000 - $25,000 annually

- Vulnerability scanning: $2,000 - $8,000 annually

- Security tools and infrastructure: $10,000 - $50,000 annually

Level 4 Compliance Costs:

- SAQ self-completion: $500 - $5,000 annually

- Basic security tools: $2,000 - $10,000 annually

- Training and documentation: $1,000 - $5,000 annually

Best Practices for Achieving and Maintaining Compliance

Start with Data Flow Mapping Understanding exactly how cardholder data moves through your systems is crucial for determining appropriate security controls and selecting the right SAQ type.

Implement Network Segmentation Isolating systems that handle cardholder data reduces compliance scope and simplifies security management. Proper segmentation can significantly reduce both compliance costs and security risks.

Choose the Right Payment Solutions Using tokenization, point-to-point encryption, and outsourced payment processing can dramatically reduce PCI scope and simplify compliance efforts.

Maintain Continuous Monitoring PCI compliance isn't a one-time achievement but an ongoing process. Regular monitoring, testing, and updates ensure sustained compliance and security effectiveness.

Document Everything Comprehensive documentation of security policies, procedures, and controls is essential for compliance validation and helps maintain consistency across your organization.

Determining Your Compliance Level

Your PCI compliance level is determined by the highest transaction volume across all card brands within a 12-month period. Key considerations include:

- Count all transactions, not just successful ones

- Include transactions across all business locations and channels

- Consider acquisitions and mergers that might change your volume

- Review transaction volumes annually, as levels can change

Working with Qualified Professionals

Qualified Security Assessors (QSAs): Required for Level 1 merchants and optional for others, QSAs provide expert assessment services and can help optimize compliance strategies.

Approved Scanning Vendors (ASVs): These specialized companies provide the quarterly vulnerability scans required for most compliance levels.

Payment Processors: Many processors offer compliance support services and can help businesses choose solutions that minimize PCI scope.

Conclusion

PCI DSS compliance levels provide a risk-based framework that scales security requirements with transaction volume and business size. While compliance requires ongoing investment and attention, achieving PCI DSS compliance is vital for securing cardholder data and upholding customer trust.

Understanding your compliance level is the first step toward implementing appropriate security measures that protect both your business and your customers. Whether you're a Level 4 merchant completing a simple SAQ or a Level 1 enterprise undergoing comprehensive assessment, the principles remain the same: protect cardholder data, maintain security awareness, and view compliance as an ongoing journey rather than a destination.

By investing in proper PCI DSS compliance, businesses not only meet regulatory requirements but also build a foundation of trust that supports long-term growth and customer loyalty in an increasingly digital marketplace. The cost of compliance is always less than the cost of a breach, making PCI DSS adherence one of the most important investments a business can make in today's payment landscape.

Get started with your PCI DSS today using our compliance management service. Regulance uses AI to automate compliance and helps you to get things done accurately and faster. Schedule a demo here with our compliance experts to learn more.