PCI ROC or PCI AOC: Which PCI Compliance Report Do You Need?

Introduction

In the recent digital economy, where billions of payment card transactions occur daily, protecting cardholder data has become a critical responsibility for businesses of all sizes. The Payment Card Industry Data Security Standard (PCI DSS) serves as the cornerstone framework ensuring that organizations handling credit card information maintain robust security measures. However, compliance with PCI DSS is about demonstrating that compliance through proper documentation. This is where PCI ROC (Report on Compliance) and PCI AOC (Attestation of Compliance) come in.

These two documents represent different levels of compliance validation, each serving distinct purposes within the PCI DSS ecosystem. While many business owners and IT professionals have heard these terms, there's often confusion about what each document entails, who needs them, and how they differ from one another. Understanding the distinction between PCI ROC and PCI AOC is essential for organizations accepting payment cards, as using the incorrect documentation approach can result in non-compliance penalties, increased transaction fees, or even the loss of payment processing privileges.

This guide will walk you through everything you need to know about PCI ROC and PCI AOC, helping you navigate the compliance landscape with confidence and ensure your business meets all necessary requirements while protecting your customers' sensitive payment information.

What is PCI ROC (Report on Compliance)?

The PCI ROC, or Report on Compliance, is a comprehensive document that provides detailed evidence of an organization's compliance with all applicable PCI DSS requirements. This formal report is prepared by a Qualified Security Assessor (QSA); an independent, certified professional authorized by the PCI Security Standards Council to validate PCI DSS compliance.

A PCI ROC is an exhaustive document, typically ranging from 100 to over 300 pages depending on the complexity of the organization's payment card environment. It contains in-depth analysis of the merchant or service provider's systems, processes, policies, and security controls. The report methodically addresses each of the 12 major requirements and approximately 300+ sub-requirements of the PCI DSS framework, providing detailed findings for each control.

The PCI ROC includes several critical components: an executive summary outlining the scope of the assessment and overall compliance status; a detailed description of the cardholder data environment (CDE); network diagrams illustrating data flow; documentation of all systems, applications, and processes involved in payment card processing; and specific evidence demonstrating compliance with each PCI DSS requirement. The QSA also documents any compensating controls implemented when standard requirements cannot be met directly.

One of the most significant aspects of the PCI ROC is its requirement for on-site assessments. QSAs conduct thorough examinations of the physical and technical environments, interview key personnel, review documentation and policies, examine system configurations, and validate security controls through testing. This rigorous process ensures that compliance isn't merely theoretical but is actively implemented and maintained.

The PCI ROC must be completed annually, and organizations subject to this requirement must engage a QSA to perform the assessment. The resulting report is then submitted to acquiring banks and payment card brands as proof of compliance, providing assurance that the organization maintains appropriate security measures to protect cardholder data throughout the year.

What is PCI AOC (Attestation of Compliance)?

The PCI AOC, or Attestation of Compliance, is a shorter, more streamlined document compared to the ROC. It serves as a formal statement confirming that an organization has completed a PCI DSS assessment and is compliant with the applicable requirements. The AOC is essentially a summary document typically only 3-6 pages that executives sign to attest to their organization's compliance status.

There are different types of AOCs depending on the validation method used. Some AOCs accompany a PCI ROC when a QSA conducts the assessment, serving as the executive attestation to complement the detailed technical report. Other AOCs are standalone documents used with Self-Assessment Questionnaires (SAQs), where merchants conduct their own compliance evaluation and attest to the results without external validation.

A PCI AOC contains several key sections: identification information about the merchant or service provider; the scope of the assessment including which SAQ type was used or confirmation that a ROC was completed; dates of the assessment and attestation; acknowledgment of responsibility for maintaining PCI DSS compliance; and executive signature affirming the accuracy of the compliance statement. The AOC also identifies which PCI DSS version was assessed against and specifies any services or functions that were excluded from the assessment scope.

The fundamental purpose of the PCI AOC is to provide acquiring banks, payment processors, and payment card brands with a quick reference document confirming compliance status. While it doesn't contain the granular detail found in a ROC or SAQ, the AOC carries significant weight because it includes executive-level attestation. By signing the document, company leadership acknowledges their organization's compliance status and responsibility for maintaining security controls.

Organizations completing SAQs typically submit the AOC along with the completed questionnaire. Those undergoing QSA assessments submit the AOC alongside their PCI ROC. In both cases, the AOC serves as the formal compliance declaration that payment brands and acquiring banks require, making it an essential component of the compliance validation process regardless of the assessment method used.

Key Differences Between PCI ROC and AOC

Understanding the distinctions between PCI ROC and PCI AOC is crucial for proper compliance management. These documents differ significantly in purpose, scope, length, creation process, and applicability.

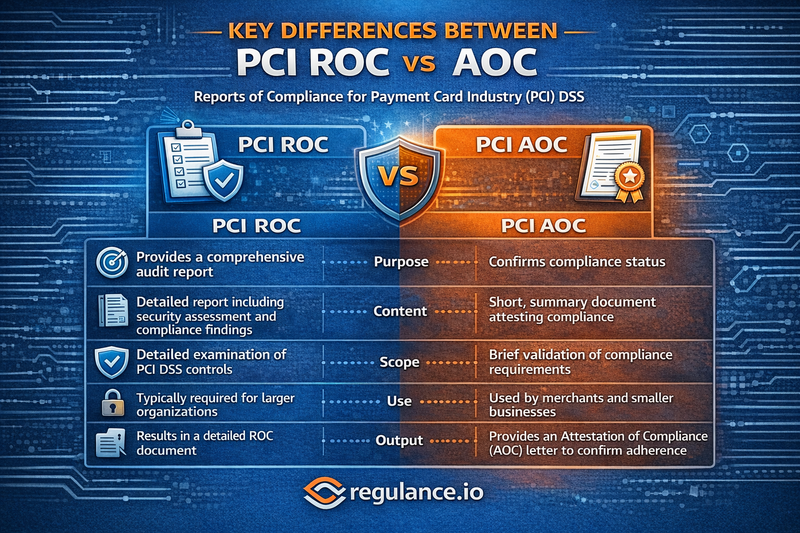

Document Complexity and Length: The most obvious difference is document size. A PCI ROC is an extensive technical report spanning hundreds of pages with detailed evidence and findings, while a PCI AOC is a brief summary document typically under ten pages that simply attests to compliance status.

Who Prepares the Document: A PCI ROC must be prepared exclusively by a Qualified Security Assessor (QSA), an independent third party certified by the PCI Security Standards Council. In contrast, a PCI AOC can be completed by either a QSA (when accompanying a ROC) or by the merchant itself (when accompanying a self-assessment).

Level of Detail: The PCI ROC provides granular analysis of every security control, including testing methodology, evidence reviewed, findings for each requirement, and documentation of any gaps or compensating controls. The PCI AOC contains minimal detail, primarily identifying which assessment type was completed and providing executive attestation of the results.

Required Evidence: A PCI ROC includes comprehensive supporting documentation such as network diagrams, policy documents, system configurations, vulnerability scan results, penetration testing reports, and photographic evidence. An AOC requires no supporting evidence, it's a standalone attestation document.

Assessment Method: The PCI ROC requires rigorous on-site assessments with interviews, system reviews, and validation testing conducted by the QSA. An AOC accompanying a self-assessment may not involve any external validation, relying instead on the organization's own evaluation.

Cost Implications: Obtaining a PCI ROC involves significant expense typically $15,000 to $50,000 or more due to QSA engagement fees. A self-generated AOC with an SAQ costs substantially less, often just the administrative time to complete the questionnaire.

Applicability: PCI ROC is mandatory only for Level 1 merchants and service providers (those processing the highest transaction volumes), while PCI AOC is required for all compliance validation methods, regardless of merchant level. Every compliant organization needs an AOC, but only the largest organizations need a ROC.

Importance of PCI ROC for Businesses

For organizations required to obtain a PCI ROC, this document serves multiple critical functions that extend far beyond simple regulatory compliance.

Demonstrated Due Diligence: The PCI ROC provides irrefutable evidence that an organization has invested in comprehensive security assessments. This demonstration of due diligence can be invaluable in legal situations, reducing liability if a breach occurs by showing the organization took reasonable security measures.

Comprehensive Security Validation: Unlike self-assessments, the PCI ROC involves independent expert analysis of security controls. QSAs bring specialized knowledge and objective perspectives, often identifying vulnerabilities or weaknesses that internal teams might overlook. This third-party validation ensures security measures are genuinely effective, not just theoretically compliant.

Stakeholder Confidence: Major acquiring banks, payment processors, and payment card brands require PCI ROC from high-volume processors because it provides assurance that these organizations which represent the greatest potential risk due to transaction volume maintain appropriate security. The ROC's comprehensiveness instills confidence among business partners and customers.

Detailed Security Roadmap: The PCI ROC provides detailed findings and recommendations. Even when organizations are compliant, QSAs often note opportunities for security enhancement. These insights become a roadmap for continuous improvement, helping organizations strengthen their security posture beyond minimum requirements.

Risk Management: For enterprises processing millions of transactions, the financial and reputational risks of a breach are enormous. The rigorous assessment process behind the PCI ROC helps identify and address vulnerabilities before they can be exploited, serving as a critical risk management tool.

Regulatory Requirement: For Level 1 merchants and service providers, the PCI ROC is mandatory. Failure to produce an annual ROC can result in penalties, increased transaction fees, or loss of payment processing privileges, making it a business-critical document.

The investment in obtaining a PCI ROC, while substantial, ultimately protects businesses from far greater costs associated with data breaches, which can include forensic investigation expenses, legal fees, regulatory fines, customer notification costs, credit monitoring services, and devastating reputational damage.

Importance of PCI AOC for Businesses

The PCI AOC, despite its brevity, holds significant importance for businesses at all levels of payment card processing.

Universal Compliance Proof: Regardless of merchant level or assessment type, every organization demonstrating PCI DSS compliance must submit an AOC. This makes it the universal currency of compliance validation, accepted by all acquiring banks and payment card brands as formal proof of compliance status.

Executive Accountability: The AOC requires signature from C-level executives or business owners, establishing clear accountability for compliance. This executive attestation ensures that PCI compliance isn't merely an IT concern but is recognized as a business-critical issue at the highest organizational levels.

Simplified Verification: For acquiring banks and payment processors managing thousands of merchant relationships, the AOC provides a standardized, easily reviewable document for compliance verification. Rather than reviewing hundreds of pages of technical details, they can quickly confirm compliance status through the concise AOC.

Cost-Effective Compliance Documentation: For smaller merchants eligible for self-assessment, the AOC paired with an SAQ provides a much more affordable compliance validation path than a full ROC. This accessibility ensures that even small businesses can demonstrate compliance without prohibitive costs.

Annual Compliance Tracking: The AOC includes specific dates for the assessment and attestation, creating a clear compliance timeline. Acquiring banks use these dates to track whether merchants are maintaining current compliance status and to identify when re-validation is due.

Business Relationship Requirement: Many payment processors and acquiring banks will not establish or maintain business relationships with merchants who cannot provide a current AOC. The document is often a contractual requirement, making it essential for maintaining payment processing capabilities.

Reduced Transaction Fees: Some acquiring banks offer preferential transaction fees to merchants who can demonstrate current PCI compliance through a valid AOC. The cost savings from reduced fees can be substantial, particularly for businesses processing significant transaction volumes.

For businesses of all sizes, the PCI AOC represents the formal commitment to cardholder data security and serves as the essential document for maintaining payment processing privileges and business credibility in the payment card ecosystem.

Who Needs PCI ROC vs. PCI AOC?

The distinction between who needs a PCI ROC versus who can use a PCI AOC with self-assessment is primarily determined by merchant level and transaction volume, though other factors may apply.

PCI ROC Requirements:

Level 1 merchants; those processing over 6 million Visa or Mastercard transactions annually across all channels, must obtain an annual PCI ROC conducted by a QSA. Level 1 service providers that store, process, or transmit cardholder data on behalf of other organizations also require annual ROC validation. Additionally, any merchant or service provider that has suffered a data breach may be required to undergo ROC assessment regardless of transaction volume.

PCI AOC with Self-Assessment:

Level 2 merchants (1-6 million transactions annually) typically complete a Self-Assessment Questionnaire (SAQ) paired with an AOC, though some acquiring banks may require QSA validation. Level 3 merchants (20,000-1 million e-commerce transactions annually) generally use SAQ and AOC. Level 4 merchants (fewer than 20,000 e-commerce transactions or less than 1 million total transactions annually) complete an SAQ with AOC. These smaller merchants represent the vast majority of businesses accepting payment cards.

Special Circumstances:

Some acquiring banks impose stricter requirements than the minimum standards, requiring QSA-validated assessments for merchants below Level 1 thresholds. Merchants in high-risk industries may face enhanced requirements. Organizations experiencing rapid growth should monitor their transaction volumes, as crossing thresholds may change their validation requirements mid-year. International businesses must consider requirements from multiple payment card brands, which may have varying thresholds.

Service Provider Considerations:

Service providers face different categorizations. Those processing large volumes or providing critical services like payment gateways, processors, or hosting providers typically require ROC validation regardless of their direct transaction processing levels, as they impact the security of numerous merchants.

The key principle is that higher transaction volumes and greater potential impact on the payment card ecosystem correspond with more rigorous validation requirements. Businesses should verify their specific requirements with their acquiring bank, as these institutions ultimately determine what documentation is acceptable for their merchant portfolios.

The Process of Obtaining PCI ROC and AOC

Understanding the processes for obtaining these compliance documents helps organizations plan appropriately and allocate necessary resources.

Obtaining a PCI ROC:

The process begins with selecting a Qualified Security Assessor (QSA) from the PCI Security Standards Council's list of approved assessors. Organizations should evaluate QSAs based on industry expertise, assessment approach, and cost. Once engaged, the QSA conducts a scoping exercise to determine which systems, networks, and processes are in scope for the assessment.

Pre-assessment preparation involves gathering documentation, including network diagrams, security policies, system inventories, and evidence of security controls. The organization completes vulnerability scans from an Approved Scanning Vendor (ASV) if applicable. The QSA then conducts on-site assessment activities including interviews with personnel across IT, security, and business functions; technical examination of systems, networks, and applications; review of policies, procedures, and documentation; and validation testing of security controls.

Following field work, the QSA analyzes findings and prepares the draft ROC, which the organization reviews for factual accuracy. Any identified gaps must be remediated before the final ROC is issued. Once remediation is complete and verified, the QSA produces the final PCI ROC and accompanying AOC. The organization submits these documents to acquiring banks and payment card brands, maintaining copies for internal records.

The entire process typically takes 2-4 months depending on organization size, complexity, and preparedness. Annual ROC renewal begins several months before the current ROC expires to ensure continuous compliance.

Obtaining a PCI AOC with Self-Assessment:

For organizations eligible for self-assessment, the process is more straightforward. First, determine which SAQ type applies based on payment processing methods (there are currently nine different SAQ types, each designed for specific merchant scenarios). Download the appropriate SAQ from the PCI Security Standards Council website.

Complete the questionnaire honestly and thoroughly, documenting compliance with applicable requirements. Gather supporting evidence for your records, though it's not submitted with the SAQ. Remediate any identified gaps before attesting to compliance. Complete the corresponding AOC, including executive signature. Submit both the completed SAQ and AOC to your acquiring bank or payment processor. Completing an SAQ and AOC typically takes days to weeks rather than months, though organizations new to PCI compliance may need additional time to implement required controls.

Best Practices for Both Processes:

Treat compliance as an ongoing program rather than an annual event. Maintain continuous compliance monitoring and documentation. Engage qualified professionals when needed even for self-assessments, many organizations benefit from consultant guidance. Start early, beginning the renewal process well before current compliance documentation expires. Maintain organized records of all compliance activities, evidence, and documentation throughout the year.

FAQs

What is the difference between PCI ROC and PCI AOC?

A PCI ROC is a comprehensive technical report prepared by a QSA detailing an organization's compliance with all PCI DSS requirements, while a PCI AOC is a brief attestation document signed by executives confirming compliance status. The ROC contains detailed findings and evidence; the AOC is a summary statement.

Do I need both a PCI ROC and a PCI AOC?

If your organization requires a PCI ROC (Level 1 merchants/service providers), you will receive both documents, the detailed ROC and an accompanying AOC. If you're eligible for self-assessment, you only need an AOC paired with your completed SAQ, not a ROC.

How much does a PCI ROC cost?

PCI ROC costs vary significantly based on organization size and complexity but typically range from $15,000 to $50,000 or more. Larger, more complex environments with multiple locations or intricate payment systems may cost substantially more.

How long is a PCI ROC or AOC valid?

Both documents are valid for one year from the date of assessment. Organizations must complete annual re-validation to maintain current compliance status and avoid penalties or service disruptions.

Can I complete my own PCI ROC?

No, a PCI ROC must be completed by a Qualified Security Assessor (QSA). However, eligible merchants can complete Self-Assessment Questionnaires (SAQs) with corresponding AOCs without QSA involvement.

What happens if I don't obtain required PCI compliance documentation?

Failure to provide required PCI documentation can result in monthly non-compliance fees from acquiring banks, increased transaction processing fees, restrictions on payment processing capabilities, or complete loss of ability to accept payment cards.

Which SAQ type do I need?

SAQ type depends on how you process payment cards. The PCI Security Standards Council provides an SAQ selection tool, and your acquiring bank can provide guidance. Common types include SAQ A for e-commerce using redirected payment pages, SAQ A-EP for e-commerce with some cardholder data on merchant systems, and SAQ D for all other merchants.

Do I need to be PCI compliant if I use a payment processor?

Yes. While using a compliant payment processor reduces your compliance scope, merchants remain responsible for their portion of the payment environment and must complete appropriate PCI validation based on their merchant level.

Conclusion

PCI ROC and PCI AOC represent essential components of the payment card industry's approach to data security, each serving distinct but complementary roles in the compliance ecosystem. The PCI ROC provides comprehensive, detailed validation of security controls for high-volume processors and service providers, offering rigorous third-party assessment and extensive documentation. The PCI AOC serves as the universal compliance attestation document, required regardless of assessment method, providing streamlined verification for stakeholders throughout the payment chain.

Understanding which document your organization needs, how to obtain it, and what it represents is fundamental to maintaining payment processing capabilities and protecting cardholder data. The distinction between these documents reflects the risk-based approach embedded within PCI DSS, scaling validation rigor to match the potential impact of security failures.

Whether your organization requires the extensive PCI ROC process or can utilize self-assessment with an AOC, the underlying principle remains consistent: protecting cardholder data through robust security controls and demonstrating that commitment through proper validation and documentation. The challenges of PCI compliance are real, but so are the consequences of non-compliance and the risks of inadequate security.

As payment technologies evolve and cyber threats grow more sophisticated, PCI compliance requirements will continue adapting. Organizations that treat compliance as an ongoing security program rather than an annual checkbox exercise will find themselves better positioned not only to meet requirements but to genuinely protect their customers and their business from the devastating consequences of payment card data breaches.

Ready to streamline your PCI compliance journey? Contact Regulance today to discover how we can transform your compliance challenges into competitive advantages, protecting your business while enabling growth in the digital payment ecosystem.