PCI DSS Level 4: What Does It Really Mean for Your Business and How Do You Stay Compliant?

Introduction

Payment card security has become a cornerstone of consumer trust and business integrity. Every time a customer swipes, taps, or enters their card details online, they're placing their faith in businesses to protect their sensitive financial information. This trust is backed by strict industry standards designed to safeguard cardholder data from increasingly sophisticated cyber threats.

The Payment Card Industry Data Security Standard, commonly known as PCI DSS, represents the gold standard in payment security protocols. This comprehensive framework was developed collaboratively by major credit card companies including Visa, Mastercard, American Express, Discover, and JCB to create a unified approach to securing payment transactions. Within this framework exists a tiered compliance system that categorizes merchants and service providers based on their transaction volumes, with each level carrying specific requirements and obligations.

PCI DSS Level 4 sits at one end of this spectrum, representing smaller merchants who process the fewest number of transactions annually. While these businesses may be modest in size compared to enterprise-level corporations, their responsibility to protect customer payment data remains just as critical. Understanding what PCI DSS Level 4 entails, who it applies to, and how to maintain compliance can mean the difference between building customer confidence and facing devastating security breaches that could permanently damage a small business's reputation and financial stability.

This comprehensive guide explores everything you need to know about PCI DSS Level 4 compliance, from its precise definition and key requirements to the advantages of maintaining certification and the transformative role that automation plays in simplifying the compliance journey for smaller merchants.

What is PCI DSS Level 4?

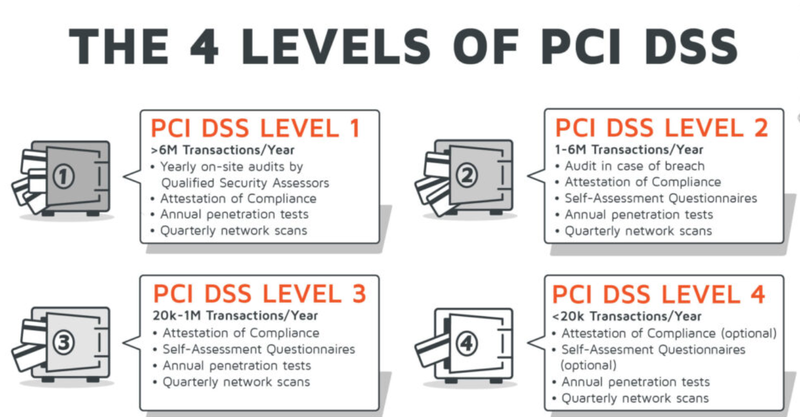

PCI DSS Level 4 represents the entry tier in the Payment Card Industry Data Security Standard compliance hierarchy. Specifically, Level 4 applies to merchants who process fewer than 20,000 Visa or Mastercard e-commerce transactions annually, or any merchant processing up to one million total transactions per year across all channels combined. This classification makes Level 4 the most common compliance level, encompassing millions of small businesses, independent retailers, local service providers, and emerging e-commerce ventures worldwide.

The level system within PCI DSS exists to create proportionate compliance requirements that match the risk profile of different business sizes. Larger merchants processing millions of transactions annually face more stringent validation requirements, including mandatory on-site security assessments by Qualified Security Assessors. Level 4 merchants, conversely, typically have more streamlined validation processes that reflect their smaller operational scale and lower overall transaction volumes.

However, it's crucial to understand that Level 4 designation doesn't mean reduced security standards, the fundamental PCI DSS requirements remain consistent across all levels. What differs is the validation methodology. Level 4 merchants generally complete an annual Self-Assessment Questionnaire, or SAQ, rather than undergoing extensive third-party audits. This SAQ is a detailed validation tool that allows merchants to evaluate their own compliance with PCI DSS requirements through a comprehensive series of questions covering security policies, procedures, and technical implementations.

The specific SAQ version a Level 4 merchant must complete depends on their payment processing methods. For instance, a merchant using only standalone card terminals with no electronic storage of cardholder data would complete a different, often shorter SAQ than an e-commerce business that processes card-not-present transactions through their website. Common SAQ types for Level 4 merchants include SAQ A for e-commerce merchants who fully outsource payment processing, SAQ A-EP for e-commerce merchants with more control over the payment page, and SAQ D for merchants with more complex payment environments.

Beyond transaction volume, merchants can also be elevated to higher compliance levels if they've experienced a data breach or compromise. This elevation serves as both a remediation measure and an accountability mechanism, requiring enhanced scrutiny of security practices following a security incident. Therefore, maintaining robust security practices at Level 4 isn't just about meeting current requirements, it's about preventing circumstances that could force reclassification to more demanding compliance tiers.

What Are the Key Requirements Of PCI DSS Level 4?

While Level 4 merchants may use self-assessment for validation, they must still adhere to the comprehensive security framework established by the twelve core PCI DSS requirements. These requirements are organized into six overarching objectives that together create a defense-in-depth approach to payment security.

Build and Maintain a Secure Network and Systems

The foundation of PCI DSS compliance begins with establishing secure network infrastructure. Merchants must install and maintain firewall configurations that protect cardholder data environments from unauthorized access. This includes properly configured firewalls at all network perimeters and between any systems that store, process, or transmit cardholder data. Additionally, merchants must avoid using vendor-supplied default passwords and security parameters for systems and applications. Default credentials are among the most exploited vulnerabilities in cybersecurity, making this requirement critical for preventing unauthorized access to payment systems.

Protect Cardholder Data

Data protection forms the heart of PCI DSS compliance. Merchants must protect stored cardholder data through encryption, truncation, masking, and hashing techniques. The standard specifically prohibits storing sensitive authentication data after authorization, including the full magnetic stripe data, card verification codes, and PIN data. When cardholder data must be transmitted across public networks, strong cryptography and security protocols like TLS must be implemented to prevent interception by malicious actors. This requirement has become increasingly important as businesses adopt cloud services and remote work arrangements that involve data transmission across various network environments.

Maintain a Vulnerability Management Program

Cyber threats evolve constantly, making ongoing vulnerability management essential. Merchants must deploy and regularly update anti-virus software on all systems commonly affected by malware. Additionally, they must develop and maintain secure systems and applications by applying security patches promptly and following secure coding practices for any custom payment applications. This includes establishing processes for identifying newly discovered security vulnerabilities and assigning risk rankings to prioritize remediation efforts based on potential impact.

Implement Strong Access Control Measures

Limiting access to cardholder data is a fundamental security principle embodied in several PCI DSS requirements. Access must be restricted based on business need-to-know, meaning only personnel whose jobs require access to cardholder data should have such access. Each person with computer access must be assigned a unique identifier to ensure accountability and traceability of actions. Physical access to cardholder data must also be restricted, requiring appropriate physical security controls for facilities, devices, and paper records containing sensitive payment information.

Regularly Monitor and Test Networks

PCI DSS requires merchants to track and monitor all access to network resources and cardholder data through logging mechanisms that record user activities, exceptions, and security events. These logs must be reviewed regularly to detect anomalies or suspicious activities. Additionally, security systems and processes must be tested regularly through vulnerability scans, penetration testing, and security assessments to identify weaknesses before attackers can exploit them.

Maintain an Information Security Policy

Finally, merchants must establish, publish, maintain, and disseminate a comprehensive information security policy that addresses all PCI DSS requirements for all personnel. This policy creates the governance framework that ensures security isn't just a technical concern but an organizational priority embedded in business processes and employee behaviors. The policy should be reviewed annually and updated as needed to address new threats, technologies, and business changes.

For Level 4 merchants, implementing these requirements often means working closely with payment processors, point-of-sale vendors, and technology providers who can help create secure payment environments without requiring extensive in-house security expertise. Many Level 4 merchants significantly reduce their compliance scope by outsourcing payment processing to PCI-compliant third-party providers, thereby limiting the systems and processes they must secure directly.

What Are the Advantages Of PCI DSS Level 4?

Achieving and maintaining PCI DSS Level 4 compliance delivers numerous tangible benefits that extend far beyond simply meeting industry obligations. These advantages contribute directly to business sustainability, growth potential, and competitive positioning in increasingly security-conscious markets.

Enhanced Customer Trust and Confidence

In an era where data breaches regularly make headlines, customers have become increasingly selective about where they conduct business. PCI DSS compliance serves as a visible commitment to protecting customer payment information, building trust that translates directly into customer loyalty and positive brand perception. When customers see that a business takes payment security seriously, they're more likely to complete transactions, return for future purchases, and recommend the business to others. This trust factor can be particularly valuable for small businesses competing against larger retailers with more established reputations.

Reduced Risk of Data Breaches

The financial and reputational costs of data breaches can be catastrophic for small businesses. Studies consistently show that many small businesses never recover from significant security incidents, with costs including forensic investigations, legal fees, regulatory fines, customer notification expenses, and lost business far exceeding their ability to absorb such impacts. PCI DSS compliance implements proven security controls that dramatically reduce breach risk by addressing the most common attack vectors cybercriminals exploit. By following the standard's requirements, Level 4 merchants create multiple layers of defense that make successful attacks significantly more difficult.

Avoidance of Penalties and Fines

Non-compliance with PCI DSS can result in substantial financial penalties imposed by payment card brands and acquiring banks. These fines can range from thousands to hundreds of thousands of dollars depending on the severity and duration of non-compliance, creating existential threats for small businesses operating on tight margins. Additionally, merchants experiencing breaches while non-compliant face even steeper penalties and may lose their ability to accept card payments entirely. Maintaining Level 4 compliance avoids these costly consequences and ensures uninterrupted payment processing capabilities.

Improved Operational Security

The security practices required for PCI DSS compliance don't just protect payment data; they create broader operational security improvements that benefit the entire business. Implementing firewalls, access controls, logging systems, and vulnerability management processes strengthens defenses against all types of cyber threats, not just payment-related attacks. These security enhancements protect other business-critical information including employee records, business intelligence, customer contact information, and proprietary data that could be valuable to competitors or criminals.

Competitive Differentiation

PCI DSS compliance can serve as a powerful differentiator in crowded markets. Many customers actively seek out businesses that demonstrate commitment to security, particularly for online transactions where payment data is transmitted electronically. Displaying compliance certifications and security badges on websites and marketing materials signals professionalism and attention to detail that sets compliant merchants apart from competitors who may be cutting corners on security. For businesses pursuing partnerships, contracts, or marketplace participation, PCI DSS compliance is increasingly becoming a prerequisite rather than an optional credential.

Streamlined Payment Processing Relationships

Payment processors, acquiring banks, and payment service providers look favorably upon compliant merchants because they represent lower risk. Compliant merchants may benefit from more favorable processing rates, faster approval for services, and greater flexibility in payment options offered. Conversely, non-compliant merchants may face higher fees, more restrictive terms, or difficulty establishing relationships with reputable payment partners. Maintaining Level 4 compliance creates smoother business relationships throughout the payment ecosystem.

Foundation for Business Growth

As businesses grow and transaction volumes increase, maintaining established compliance practices makes transitions to higher PCI DSS levels much smoother. A Level 4 merchant that has consistently maintained compliance and developed strong security habits is well-positioned to scale operations without the disruptive scramble to implement security controls retroactively. This compliance foundation supports sustainable growth trajectories that don't compromise security or create compliance gaps during expansion periods.

The Effect of Automation on PCI DSS Level 4

The emergence of sophisticated automation technologies has fundamentally transformed how Level 4 merchants approach PCI DSS compliance, making what was once a daunting administrative burden into a manageable, streamlined process that fits naturally into small business operations.

Automated Vulnerability Scanning

Manual vulnerability assessments require specialized expertise and significant time investments that many small businesses simply cannot afford. Automated vulnerability scanning tools continuously monitor systems for known security weaknesses, misconfigurations, and outdated software that could be exploited by attackers. These tools generate regular reports highlighting specific vulnerabilities ranked by severity, allowing even non-technical business owners to understand their security posture and prioritize remediation efforts. Many scanning solutions now integrate directly with patch management systems, creating closed-loop processes where identified vulnerabilities trigger automatic updates when appropriate.

Continuous Compliance Monitoring

Traditional compliance approaches involved periodic assessments that created point-in-time snapshots of security status, leaving extended periods where compliance drift could occur unnoticed. Automation enables continuous monitoring that tracks compliance status in real-time, alerting merchants immediately when configurations change or controls fail. This continuous visibility transforms compliance from an annual event into an ongoing operational state, significantly reducing the risk that non-compliance will persist undetected until the next formal assessment. For Level 4 merchants juggling multiple business responsibilities, automated monitoring provides peace of mind without requiring constant manual oversight.

Simplified Evidence Collection and Documentation

One of the most time-consuming aspects of PCI DSS compliance involves gathering evidence to demonstrate that required controls are implemented and functioning effectively. Automation tools can automatically collect logs, screenshots, configuration files, and other evidence needed to complete Self-Assessment Questionnaires and respond to auditor inquiries. These systems maintain organized repositories of compliance documentation that are always current and easily accessible, eliminating the frantic scrambling that often preceded compliance assessments in the past. Some advanced platforms can even pre-populate SAQ responses based on collected evidence, reducing completion time from weeks to hours.

Automated Policy Management and Employee Training

Maintaining security policies and ensuring employees understand their responsibilities presents ongoing challenges, especially for businesses with limited HR resources and staff turnover. Automated policy management platforms distribute policies electronically, track employee acknowledgment, schedule regular reviews, and automatically prompt updates when requirements change. Similarly, automated training systems deliver security awareness content, track completion, and provide refresher training on regular schedules. These automation capabilities ensure the human element of compliance receives adequate attention without becoming an administrative nightmare.

Integration with Payment Processing Systems

Modern payment processing solutions increasingly incorporate compliance automation features directly into their platforms. Tokenization systems automatically replace sensitive card data with non-sensitive tokens throughout business systems, dramatically reducing PCI DSS scope by ensuring actual card numbers never touch merchant environments. Point-to-point encryption encrypts data from the moment cards are read, preventing interception during transmission. These integrated security features provide robust protection while requiring minimal merchant intervention, making sophisticated security accessible to businesses without dedicated IT staff.

Cost Reduction and Resource Optimization

Perhaps the most significant impact of automation for Level 4 merchants is the dramatic reduction in compliance costs and resource requirements. Tasks that once required hiring expensive consultants or diverting staff from revenue-generating activities can now be handled through affordable automation platforms designed specifically for small business needs. This cost-effectiveness makes consistent compliance sustainable even for merchants operating on tight budgets, removing the temptation to skip assessments or let compliance lapse due to resource constraints.

Scalability and Future-Proofing

Automation platforms scale effortlessly as businesses grow, accommodating increased transaction volumes, additional locations, and expanded payment channels without requiring proportional increases in compliance effort. When a Level 4 merchant's growth eventually necessitates advancement to Level 3 or higher, the compliance infrastructure is already in place and simply needs enhancement rather than complete rebuilding. This scalability ensures that security and compliance support business growth rather than constraining it.

The automation revolution has democratized PCI DSS compliance, making enterprise-grade security accessible to even the smallest merchants. By leveraging these technologies, Level 4 merchants can maintain robust compliance programs that rival those of much larger organizations, all while focusing their limited resources on core business activities that drive growth and profitability.

Frequently Asked Questions (FAQs)

How often must Level 4 merchants validate PCI DSS compliance?

Level 4 merchants must validate their PCI DSS compliance annually by completing the appropriate Self-Assessment Questionnaire and, in many cases, submitting an Attestation of Compliance to their acquiring bank. Additionally, quarterly vulnerability scans by an Approved Scanning Vendor may be required depending on the merchant's environment and the specific SAQ type. However, it's important to understand that compliance is an ongoing operational state, not just an annual event. Merchants must maintain the security controls and practices documented in their SAQ throughout the year, even though formal validation occurs annually.

What happens if a Level 4 merchant experiences a data breach?

A data breach can have severe consequences for Level 4 merchants. Immediate steps include containing the breach, notifying the acquiring bank and payment brands, conducting forensic investigations, and potentially notifying affected cardholders. Financially, merchants may face forensic investigation costs, legal fees, fines from payment card brands, increased processing fees, and potential lawsuits. Following a breach, merchants are typically elevated to a higher validation level requiring more stringent compliance assessments and may face mandatory third-party audits. Some merchants lose their ability to accept card payments entirely if breach circumstances reveal egregious security failures.

Can Level 4 merchants reduce their compliance scope?

Yes, scope reduction represents one of the most effective strategies for simplifying PCI DSS compliance. Merchants can minimize scope by outsourcing payment processing to PCI-compliant third-party providers, implementing point-to-point encryption that protects data from the point of interaction, using tokenization to replace sensitive data with non-sensitive equivalents, segmenting networks to isolate systems that handle cardholder data, and eliminating unnecessary storage of payment information. Many Level 4 merchants qualify for simpler SAQ types by adopting these scope reduction approaches, dramatically decreasing the complexity and effort required for compliance validation.

Is PCI DSS compliance legally required?

PCI DSS is not a government-mandated legal requirement in most jurisdictions, but rather an industry standard imposed by payment card brands as a contractual obligation. However, refusing to comply isn't a realistic option for businesses that want to accept card payments. Payment processors and acquiring banks require compliance as a condition of providing services, and non-compliance results in penalties, increased fees, or termination of payment processing privileges. Additionally, various data protection laws and regulations may incorporate PCI DSS by reference or establish similar security requirements, creating indirect legal obligations. Practically speaking, PCI DSS compliance should be considered mandatory for any business accepting payment cards.

Do Level 4 merchants need to hire a security consultant?

While not required, many Level 4 merchants find value in working with security consultants or managed security service providers, particularly when initially establishing compliance programs or addressing complex technical environments. However, advances in automation and the availability of simplified compliance solutions designed for small businesses have made self-directed compliance increasingly feasible. Merchants using fully outsourced payment processing with limited cardholder data interaction can often achieve compliance through their service providers' guidance and automated tools. The decision to engage consultants should be based on the complexity of the payment environment, internal technical expertise, and available resources.

What's the difference between PCI DSS compliance and PCI validation?

This distinction is crucial but often misunderstood. PCI DSS compliance refers to the actual implementation and maintenance of security controls that meet all twelve requirements of the standard. Validation is the formal process of documenting and demonstrating compliance through Self-Assessment Questionnaires, attestations, and vulnerability scans. A merchant might complete validation paperwork annually but fail to maintain actual compliance throughout the year by allowing security controls to degrade, configurations to drift, or new vulnerabilities to go unaddressed. True compliance is a continuous operational state, while validation is the periodic formal documentation of that state.

Conclusion

PCI DSS Level 4 compliance represents far more than a regulatory checkbox for small merchants; it embodies a fundamental commitment to protecting the customers who trust businesses with their sensitive payment information. While Level 4 designates the entry tier of the PCI DSS framework, the importance of maintaining robust security standards at this level cannot be overstated. The overwhelming majority of businesses processing payment cards fall into Level 4, making this classification the foundation upon which global payment security depends.

The journey to PCI DSS Level 4 compliance need not be overwhelming or prohibitively expensive. Through strategic use of outsourced payment processing, scope reduction techniques, and modern automation platforms, even the smallest merchants can establish and maintain compliant environments that provide enterprise-grade security. The advantages of compliance extend well beyond avoiding penalties, delivering meaningful benefits including enhanced customer trust, reduced breach risk, competitive differentiation, and operational security improvements that protect the entire business.

As cyber threats continue to evolve and consumers become increasingly security-conscious, PCI DSS compliance will only grow more critical to business success. The merchants who embrace compliance as an operational priority rather than viewing it as an inconvenient obligation will find themselves better positioned to build customer loyalty, support sustainable growth, and navigate the complex payment security landscape with confidence.

The automation revolution has removed many of the traditional barriers that made compliance challenging for resource-constrained small businesses. Today's compliance tools deliver sophisticated security capabilities through intuitive interfaces designed for non-technical users, democratizing access to protection that was once available only to large enterprises with dedicated security teams. Level 4 merchants can now implement comprehensive compliance programs without diverting excessive resources from core business activities.

Ultimately, PCI DSS Level 4 compliance should be viewed as an investment in business longevity and customer relationships rather than a cost center. The reputational damage and financial devastation that follow data breaches far exceed the modest investments required to maintain compliance. By prioritizing payment security and embracing the standards designed to protect cardholder data, Level 4 merchants demonstrate the professionalism and responsibility that define successful businesses in the digital age.

Don't let compliance challenges hold you back, contact Regulance today to discover how we can transform your approach to payment security and help you build the customer trust that drives business success.