How Can a PCI QSA Help You Achieve PCI DSS Compliance?

Introduction

Payment card security has changed today’s business environment and it’s becoming absolutely essential. Every time a customer swipes, taps, or enters their card details, sensitive information flows through your systems. One breach can cost millions in fines, irreparable damage to your reputation, and the loss of customer trust that took years to build.

This is where PCI DSS (Payment Card Industry Data Security Standard) comes into play, and more specifically, where PCI QSAs become valuable. But what exactly is a QSA? Why do businesses need them? And how do you know if your organization requires one?

If you're a small e-commerce startup or a multinational corporation processing millions of transactions, understanding the role of a Qualified Security Assessor can be the difference between robust security compliance and costly vulnerabilities. This guide will walk you through everything you need to know about PCI QSAs, helping you navigate the complex world of payment card security with confidence.

What is a PCI QSA?

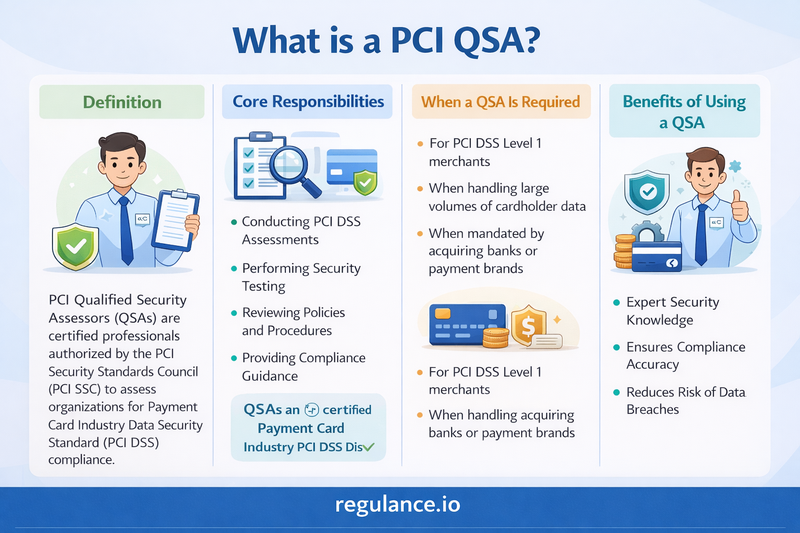

A PCI QSA, or Qualified Security Assessor, is an independent security organization that has been officially certified by the PCI Security Standards Council to validate an entity's compliance with PCI DSS requirements. Think of them as specialized auditors who possess deep expertise in payment card security standards and assessment procedures.

These QSA professionals undergo rigorous training, pass comprehensive examinations, and must demonstrate extensive knowledge of payment card processing environments, security controls, and risk assessment methodologies. The PCI Security Standards Council maintains strict qualification criteria, ensuring that only the most competent and knowledgeable organizations earn this designation.

QSAs are authorized to perform onsite assessments of organizations that store, process, or transmit cardholder data. They evaluate everything from network architecture and data storage practices to employee training programs and incident response procedures. After completing their assessment, they produce an official Report on Compliance (ROC) or Attestation of Compliance (AOC) that documents whether the organization meets all applicable PCI DSS requirements.

It's important to understand that QSAs work independently from both the payment card brands (Visa, Mastercard, American Express, etc.) and the businesses they assess. This independence is crucial, it ensures objectivity and maintains the integrity of the compliance validation process.

The QSA certification must be renewed annually, requiring ongoing training and adherence to the PCI Security Standards Council's code of professional responsibility. This ensures that QSAs stay current with evolving threats, new technologies, and updates to the PCI DSS framework itself.

What is Their Role?

The role of a PCI QSA extends far beyond simply checking boxes on a compliance form. These security professionals serve multiple critical functions that help organizations achieve and maintain payment card security.

Comprehensive Security Assessments

The primary responsibility of a QSA is conducting thorough assessments of an organization's cardholder data environment. This involves examining network segmentation, encryption protocols, access controls, vulnerability management processes, and dozens of other security requirements specified in PCI DSS. They don't just review documentation, they perform hands-on testing, interview personnel, and verify that security controls actually function as intended.

Gap Analysis and Remediation Guidance

Before the formal assessment, many QSAs provide gap analysis services to identify where an organization falls short of compliance. This pre-assessment phase is incredibly valuable because it allows businesses to address deficiencies before the official audit. QSAs can recommend specific remediation strategies, suggest appropriate security technologies, and provide roadmaps for achieving compliance.

Documentation and Reporting

After completing their assessment, QSAs prepare detailed documentation including the Report on Compliance (ROC). This comprehensive document outlines all testing procedures performed, findings discovered, and the organization's compliance status for each PCI DSS requirement. For organizations that achieve compliance, this report serves as official proof for payment card brands and acquiring banks.

Expert Consultation and Education

Beyond formal assessments, QSAs often serve as trusted advisors, helping organizations understand the nuances of PCI DSS requirements. They can clarify confusing aspects of the standard, explain how requirements apply to specific business models, and provide insights based on experience with numerous other organizations. Many QSAs also offer training programs to help internal teams develop security awareness and compliance expertise.

Bridge Between Business and Payment Brands

QSAs act as intermediaries between merchants and the payment card industry. They understand the expectations of card brands and acquiring banks, helping businesses meet these requirements in ways that make sense for their specific operational context. This translation function is invaluable for organizations navigating the sometimes complex landscape of payment card security.

Ongoing Support and Continuous Compliance

The best QSAs don't disappear after signing off on compliance. They provide ongoing support, monitoring regulatory changes, advising on new threats, and helping organizations maintain their security posture between annual assessments. This continuous relationship helps businesses avoid the costly mistake of treating compliance as a one-time checkbox exercise.

Is a QSA Necessary for Your Organization?

Not every organization that accepts payment cards needs to work with a QSA, but many do. Whether you need one depends primarily on your organization's merchant level classification and the number of transactions you process annually.

Merchant Level Classifications

Payment card brands classify merchants into four levels based on transaction volume:

Level 1 Merchants process over 6 million card transactions annually (any combination of card-present and card-not-present transactions) or have experienced a data breach. These merchants absolutely require an annual onsite assessment by a PCI QSA. There are no exceptions to this requirement.

Level 2 Merchants process between 1 million and 6 million transactions per year. These organizations typically must complete an annual Self-Assessment Questionnaire (SAQ) and may need a QSA assessment depending on their acquiring bank's requirements.

Level 3 Merchants process between 20,000 and 1 million e-commerce transactions annually. They generally complete an annual SAQ and may need quarterly network scans by an Approved Scanning Vendor (ASV), but a QSA assessment isn't usually mandatory unless required by their acquiring bank.

Level 4 Merchants process fewer than 20,000 e-commerce transactions or up to 1 million total transactions per year. These smaller merchants typically only need to complete an annual SAQ.

Beyond Transaction Volume

However, transaction volume isn't the only factor. Your acquiring bank or payment processor might require QSA validation regardless of your merchant level, especially if you've experienced a security incident, have a complex cardholder data environment, or operate in a high-risk industry.

Some organizations voluntarily engage QSAs even when not strictly required. Why? Because the expertise and validation a QSA provides can reduce insurance premiums, strengthen customer confidence, create competitive advantages, and provide assurance that security investments are properly directed.

Service Providers Have Different Rules

If your organization is a service provider that stores, processes, or transmits cardholder data on behalf of other organizations, different rules apply. Service providers processing over 300,000 transactions annually typically require annual QSA assessments regardless of other factors.

When in Doubt, Ask

The clearest answer about whether you need a QSA comes from your acquiring bank or payment processor. They establish compliance requirements for their merchants and can definitively tell you what level of validation you need. If they require QSA validation, non-compliance could result in fines, increased transaction fees, or even termination of your ability to accept payment cards.

What to Expect While Working with a QSA

Understanding the QSA assessment process helps organizations prepare effectively and maximize the value of the engagement. While specific approaches vary between QSA companies, most follow a similar framework.

Initial Scoping and Planning

The process begins with scoping, defining exactly what will be assessed. Your QSA will work with you to identify all locations, systems, networks, and processes that store, process, or transmit cardholder data. Proper scoping is crucial because it determines which PCI DSS requirements apply and how extensively they must be tested. Expect detailed conversations about your network architecture, payment processing flows, third-party connections, and data retention practices.

Pre-Assessment Readiness Review

Many QSAs offer a pre-assessment or readiness review before the formal audit. This informal evaluation identifies gaps and gives you time to remediate issues before the official assessment. While this adds time to the overall process, it significantly increases your chances of achieving compliance on the first formal attempt and avoids the costs of failed audits.

Documentation Requests

Be prepared to provide extensive documentation including network diagrams, policy documents, procedure manuals, configuration files, system inventories, vendor agreements, and evidence of security controls. QSAs need to see not just that policies exist, but that they're implemented, followed, and effective. The more organized and complete your documentation, the smoother the assessment process.

Onsite Assessment Activities

For onsite assessments, the QSA team will spend days or even weeks at your facilities conducting interviews, observing processes, testing systems, and validating controls. They'll speak with personnel at all levels, from IT administrators and developers to customer service representatives and executives. Expect configuration reviews, vulnerability scans, penetration testing, physical security inspections, and sampling of security logs and monitoring systems.

Interim Findings and Remediation

Rather than waiting until the end, good QSAs communicate findings throughout the assessment. If they discover non-compliances, they'll discuss them with you, explain the risks, and often suggest remediation approaches. You may have opportunities to address certain issues during the assessment period itself, though significant deficiencies typically require a follow-up assessment after remediation.

Report Delivery and Attestation

Once the assessment concludes, your QSA prepares the Report on Compliance (ROC) and Attestation of Compliance (AOC). The ROC is a comprehensive document often hundreds of pages detailing every requirement, testing procedure, and finding. The AOC is a shorter attestation signed by both the QSA and a company executive, confirming compliance status. These documents are submitted to your acquiring bank and, for Level 1 merchants, directly to the payment card brands.

Timeline Expectations

The entire process typically takes 2-6 months from initial engagement to final report, depending on your organization's size, complexity, and readiness. Simple environments with mature security programs might complete assessments more quickly, while complex multi-location enterprises with integration challenges may need more time.

Cost Considerations

QSA assessments aren't cheap. Costs vary widely based on scope, typically ranging from $30,000 to $500,000 or more for large, complex organizations. However, this investment should be weighed against potential breach costs which often run into millions of dollars and the value of expert guidance in building a robust security program.

Benefits of a QSA

While engaging a QSA involves significant investment of time, money, and resources, the benefits extend far beyond simply checking a compliance box.

Expert Security Validation

QSAs bring specialized expertise that most organizations don't possess internally. They've assessed dozens or even hundreds of different payment environments, giving them a unique perspective on what works, what doesn't, and where vulnerabilities commonly hide. This expertise helps identify security weaknesses that internal teams might overlook, even when those teams are highly skilled.

Risk Reduction and Breach Prevention

The assessment process itself strengthens security. By systematically evaluating every aspect of your cardholder data environment against comprehensive security standards, QSAs help identify and remediate vulnerabilities before attackers exploit them. Organizations that achieve and maintain PCI DSS compliance experience significantly fewer payment card breaches than non-compliant organizations.

Regulatory Compliance and Legal Protection

A QSA-validated compliance status provides strong evidence of due diligence should a breach occur. While PCI DSS compliance doesn't eliminate liability, it demonstrates that you took reasonable security measures. This can influence regulatory penalties, litigation outcomes, and insurance claims. Many cyber insurance policies require PCI DSS compliance or offer reduced premiums for compliant organizations.

Competitive Advantage and Customer Trust

In an era of frequent data breaches, demonstrating robust security practices sets you apart from competitors. Many enterprise customers and partners require proof of PCI DSS compliance before doing business with you. Publicly communicating your compliance status and commitment to security can strengthen customer confidence and influence purchasing decisions.

Operational Improvements

The PCI DSS framework addresses fundamental security practices that benefit your entire organization, not just payment card processing. Implementing requirements like access controls, change management, security monitoring, and incident response procedures creates operational efficiencies and reduces overall IT risk. Many organizations find that achieving PCI DSS compliance elevates their entire security program.

Avoiding Penalties and Fines

Non-compliance can be expensive. Payment card brands can impose monthly fines ranging from $5,000 to $100,000 for non-compliant Level 1 merchants. Acquiring banks may charge additional penalties, increase transaction fees, or terminate merchant agreements entirely. A QSA assessment that validates compliance eliminates these risks.

Structured Security Roadmap

Even if you don't achieve full compliance on the first assessment, the process provides a clear roadmap for security improvements. QSAs prioritize findings by risk, helping you allocate resources effectively. This structured approach prevents the common problem of randomly implementing security tools without addressing the most critical vulnerabilities first.

Ongoing Advisory Relationship

The best QSA engagements evolve into long-term partnerships. Your QSA becomes a trusted advisor who understands your business, your environment, and your security challenges. They can provide guidance on new technologies, emerging threats, regulatory changes, and strategic security initiatives, offering value far beyond annual compliance validation.

How to Choose the Right QSA

Selecting the right QSA is crucial because this partner will deeply understand your business and play a significant role in your security program. Not all QSAs are created equal, and the cheapest option is rarely the best choice.

Verify Official QSA Status

Start by confirming that the company is actually a qualified QSA. The PCI Security Standards Council maintains a public list of all qualified assessors on their website. Verify the company's listing, check their qualification status, and confirm they're authorized to perform assessments in your geographic region. Be wary of companies claiming QSA capabilities without official certification.

Industry Experience and Expertise

Look for QSAs with experience in your specific industry and business model. Payment environments vary dramatically between retail stores, e-commerce platforms, restaurants, hotels, payment processors, and other sectors. A QSA who understands your type of environment will provide more relevant guidance and conduct more efficient assessments. Ask about their experience with organizations similar to yours.

Technical Capabilities

Evaluate the QSA's technical depth. Do they have expertise with the specific technologies, platforms, and payment systems you use? Can they assess complex environments involving cloud services, mobile payments, point-to-point encryption, or tokenization? Do they stay current with emerging technologies and evolving threats? Technical competence directly impacts the quality and value of the assessment.

Reputation and References

Research the QSA's reputation within the industry. Ask for references from current and former clients, particularly those with similar environments to yours. Contact these references and ask about their experience: was the QSA responsive, knowledgeable, and practical? Did they provide valuable guidance beyond basic compliance? How did they handle challenges or disagreements?

Assessment Methodology and Approach

Understand how the QSA conducts assessments. Do they offer pre-assessment readiness reviews? How do they handle scoping and sampling? What's their approach to communicating findings? Do they provide interim reports? The best QSAs are transparent about their methodology and adapt their approach to your specific needs rather than applying a rigid one-size-fits-all process.

Communication and Partnership Philosophy

Pay attention to how the QSA communicates during the sales process, this often predicts how they'll behave during the engagement. Are they responsive to questions? Do they listen carefully and demonstrate understanding of your concerns? Do they position themselves as partners helping you build security, or as auditors simply looking for problems? The right QSA acts as an advisor, not an adversary.

Value Beyond Compliance

Consider what additional services and value the QSA provides. Do they offer training programs? Can they assist with remediation, not just identify issues? Do they provide ongoing support between annual assessments? Some QSAs offer consulting services, penetration testing, security tool evaluations, and other capabilities that can reduce your need for multiple vendors.

Cost Structure and Transparency

Understand the full cost structure upfront. What's included in the quoted price? Are travel expenses, report preparation, and follow-up consultation covered, or are these additional charges? What happens if issues are discovered and remediation is needed? Transparent, detailed proposals prevent surprises and allow accurate budget planning. Remember that the cheapest QSA may cost more in the long run if they miss critical issues or provide inadequate guidance.

Cultural Fit

Don't underestimate the importance of cultural fit. You'll work closely with your QSA, sharing sensitive information and collaborating on security decisions. Choose a partner whose style, values, and approach align with your organization's culture. A QSA who respects your business objectives while maintaining security standards creates the most productive relationship.

Availability and Commitment

Assess the QSA's availability and client load. Will you work with senior consultants or junior staff? How quickly can they respond to questions between assessments? What's their typical assessment timeline? QSAs who are overcommitted may rush assessments or provide inadequate attention to your specific needs.

FAQs

How often do I need a QSA assessment?

Level 1 merchants require annual QSA assessments. Some Level 2 merchants may also need annual assessments depending on their acquiring bank's requirements. Even when not required annually, many organizations conduct assessments every 1-3 years to validate their security program and maintain compliance confidence.

What's the difference between a QSA and an ISA?

An ISA (Internal Security Assessor) is an individual within your organization who has been trained and certified by the PCI Security Standards Council to conduct internal PCI DSS assessments. ISAs can perform self-assessments but cannot provide the official validation that QSAs deliver. Many organizations use ISAs to maintain compliance between QSA assessments.

Can a QSA help with remediation, or just assessment?

Many QSA companies offer both assessment and consulting services, though these must be kept separate to maintain independence. Your QSA can often recommend remediation approaches and may have consulting teams that can assist with implementation, but the assessment and remediation work should be performed by different individuals to avoid conflicts of interest.

What happens if we fail the QSA assessment?

If your assessment reveals non-compliances, the QSA will document these findings and typically provide a timeline for remediation. You'll need to address the issues and undergo re-testing, which may be a full reassessment or targeted validation depending on the scope of deficiencies. Your merchant agreement with your acquiring bank will determine any penalties during this remediation period.

How do I prepare for a QSA assessment?

Start by conducting an internal readiness review against PCI DSS requirements. Organize all documentation including policies, procedures, network diagrams, and evidence of security controls. Consider engaging your QSA for a pre-assessment gap analysis. Ensure key personnel understand their roles and are available during the assessment period. The more prepared you are, the smoother and more efficient the process.

Do small businesses need QSAs?

Most small businesses (Level 3 and 4 merchants) don't require QSA assessments and can use Self-Assessment Questionnaires instead. However, even small businesses can benefit from QSA consultation, particularly when implementing new payment systems or addressing complex security questions.

How long does a QSA assessment take?

The timeline varies based on organizational complexity. Simple environments might complete assessments in 3-6 weeks, while complex multi-location enterprises may need 3-6 months. Actual onsite assessment time typically ranges from a few days to several weeks depending on scope.

What's the difference between PCI DSS compliance and QSA validation?

PCI DSS compliance refers to meeting the security requirements outlined in the Payment Card Industry Data Security Standard. QSA validation is the official verification by a qualified third party that your organization has achieved this compliance. You can work toward compliance independently, but certain merchant levels require QSA validation as proof.

Can we switch QSAs?

Yes, you can change QSA companies at any time, though it's typically done at the end of an assessment cycle. Organizations switch QSAs for various reasons including cost, service quality, expertise needs, or relationship issues. When switching, ensure a smooth transition by providing your new QSA with previous reports and assessment documentation.

Are QSA fees tax-deductible?

QSA assessment fees are typically tax-deductible as ordinary business expenses related to regulatory compliance and security. However, tax treatment varies by jurisdiction and individual circumstances, so consult with your tax advisor for specific guidance.

Conclusion

Navigating payment card security in today's threat landscape is complex and challenging. A PCI QSA serves as your expert guide through this complexity, providing not just compliance validation but strategic security guidance that protects your organization, your customers, and your reputation.

While QSA assessments require significant investment, the alternative; operating without proper security validation, exposes your organization to far greater risks. Data breaches cost millions in direct expenses, regulatory fines, legal fees, and lost business. The reputational damage can take years to repair, if recovery is possible at all.

Choosing the right QSA partner transforms compliance from a checkbox exercise into an opportunity to strengthen your entire security posture. The best QSA relationships evolve into long-term partnerships where your assessor truly understands your business and helps you navigate not just current requirements but emerging challenges and opportunities.

Whether you're approaching your first PCI DSS assessment or looking to improve your existing compliance program, investing time in selecting the right QSA and building a collaborative relationship pays dividends far beyond the annual attestation. Your QSA becomes a trusted advisor, helping you make smart security investments, avoid costly mistakes, and maintain the customer trust that your business depends on.

Security is not a destination but a continuous journey. With the right QSA partner by your side, you can navigate this journey with confidence, knowing that your payment card security program meets rigorous standards and genuinely protects what matters most.

Ready to Achieve PCI DSS Compliance with Expert Guidance? Your payment card security is too important to leave to chance. Partner with Regulance and experience the difference that true expertise makes.