AOC vs ROC: What’s the Difference and Why Do They Matter in Compliance?

Introduction

Every business that accepts credit card payments faces a critical question: how do you prove your systems are secure enough to handle sensitive customer data? The answer lies in two fundamental compliance documents; the Attestation of Compliance (AOC) and the Report on Compliance (ROC). These aren't just bureaucratic paperwork. They're your passport to processing payments and your shield against costly data breaches that can destroy customer trust overnight.

Choosing between an AOC and ROC is not optional. Your transaction volume, business model, and merchant level determine which document you need. Get it wrong, and you risk hefty fines, suspended payment processing privileges, or worse; being held liable when a security incident occurs. The stakes are real, and the confusion surrounding these acronyms often leaves businesses scrambling at deadline time.

An AOC represents a self-assessment approach where you evaluate your own compliance with Payment Card Industry Data Security Standard (PCI DSS) requirements. A ROC, on the other hand, involves bringing in independent experts called Qualified Security Assessors who scrutinize every corner of your payment environment. One might cost you a few hours of internal work; the other could require months of preparation and tens of thousands of dollars. Both validate your security posture, but they do so in fundamentally different ways.

In this comprehensive guide, we'll break down everything you need to know about AOC and ROC documents, explore their differences, understand why they're essential for compliance, and examine recent updates in PCI DSS standards that affect these critical compliance tools.

What is AOC?

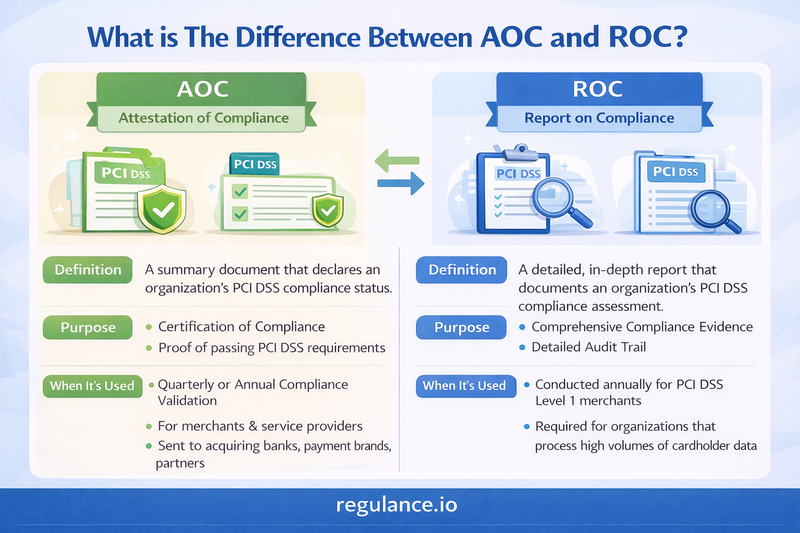

An Attestation of Compliance, commonly known as AOC, is a formal document that confirms an organization has completed a PCI DSS Self-Assessment Questionnaire (SAQ) and has met the necessary security requirements for protecting cardholder data. Think of the AOC as the official stamp of approval that declares your compliance status to acquiring banks, payment processors, and card brands.

The AOC serves as a summary document that includes several key components:

Executive Summary of Compliance Status: The AOC provides a high-level overview of your organization's compliance with PCI DSS requirements. It confirms whether your business is compliant, non-compliant, or compliant with legal exceptions.

Validation Details: This section identifies the specific SAQ version completed, the validation date, and the timeframe for which the attestation is valid (typically one year from the date of completion).

Service Provider Information: If applicable, the AOC lists any third-party service providers that impact the security of cardholder data within your environment.

Acknowledgment of Responsibility: The document requires an authorized representative from your organization to sign and acknowledge responsibility for maintaining ongoing PCI DSS compliance.

The AOC is typically associated with Self-Assessment Questionnaires, which are designed for smaller merchants or businesses with less complex payment processing environments. There are different SAQ types (SAQ A, SAQ A-EP, SAQ B, SAQ B-IP, SAQ C, SAQ D-Merchant, and SAQ D-Service Provider), each tailored to specific business models and transaction types. Regardless of which SAQ type your business completes, the corresponding AOC serves as your official declaration of compliance.

One crucial aspect of the AOC is that it's a self-reported document. Your organization assesses its own compliance status, completes the appropriate questionnaire, and then attests to the accuracy of the information provided. This doesn't mean the AOC should be taken lightly; providing false information can result in serious consequences, including fines, loss of merchant privileges, and reputational damage.

What is ROC?

A Report on Compliance, or ROC, is a comprehensive document that details the results of an extensive security assessment conducted by a Qualified Security Assessor (QSA). Unlike the self-reported AOC, the ROC is prepared by an independent third-party assessor who thoroughly examines your organization's entire cardholder data environment, security practices, and compliance with all applicable PCI DSS requirements.

The ROC is far more detailed and exhaustive than an AOC, typically spanning hundreds of pages. Here's what a thorough ROC includes:

Detailed Environmental Assessment: The ROC provides an in-depth description of your organization's cardholder data environment, including network diagrams, data flow descriptions, system components, and all locations where cardholder data is stored, processed, or transmitted.

Comprehensive Security Evaluation: Each of the 12 PCI DSS requirements is examined in meticulous detail. The QSA documents how your organization meets (or fails to meet) every sub-requirement, providing evidence, testing procedures used, and findings for each control.

Testing Methodology and Results: The report outlines the specific testing procedures employed by the assessor, including interviews conducted, systems examined, policies reviewed, and technical tests performed to validate compliance.

Compensating Controls: If your organization cannot meet a specific requirement due to legitimate technical or business constraints, the ROC documents any compensating controls implemented to mitigate the associated risk.

Remediation Plans: For any requirements where compliance gaps are identified, the ROC includes detailed remediation plans with timelines for addressing deficiencies.

Executive Summary and Conclusion: The document concludes with an overall compliance determination and recommendations for maintaining security posture.

The ROC process is rigorous and time-consuming, often taking several weeks or months to complete, depending on the complexity of your organization's environment. A QSA will conduct on-site visits, interview key personnel, review documentation, perform penetration testing, and examine technical controls before issuing the final report.

ROC validation is mandatory for organizations that process large volumes of transactions. Level 1 merchants (those processing over six million card transactions annually) and Level 1 service providers (those processing over 300,000 transactions annually) are required to undergo annual ROC assessments conducted by a QSA. Some acquiring banks may also require Level 2 merchants to obtain a ROC, depending on their specific requirements.

What is The Difference Between AOC and ROC?

While both AOC and ROC documents serve to validate PCI DSS compliance, they differ significantly in several important ways:

Assessment Method and Authority

The most fundamental difference lies in who conducts the assessment. An AOC results from a self-assessment performed by the organization itself, whereas a ROC is produced by an independent Qualified Security Assessor. The self-assessment approach of an AOC relies on the organization's internal expertise and honest evaluation, while the ROC benefits from the objective perspective and specialized knowledge of a certified external auditor.

Scope and Depth of Documentation

An AOC is a relatively brief document, typically ranging from 5 to 15 pages, that summarizes compliance status based on the completed SAQ. The ROC, conversely, is an extensive technical report that can span 200 to 400 pages or more, providing exhaustive detail on every aspect of the security assessment.

Transaction Volume Requirements

Your organization's merchant level determines which document you need. Smaller merchants processing fewer than six million transactions annually typically qualify for SAQ validation with an accompanying AOC. Larger organizations, Level 1 merchants and Level 1 service providers must undergo the more rigorous ROC process with a QSA.

Cost and Resource Investment

Completing an SAQ and generating an AOC can often be done internally with minimal cost, perhaps requiring some consulting assistance for complex environments. A ROC assessment, however, represents a significant financial investment, with QSA services typically costing between $10,000 and $100,000 or more, depending on the complexity of your environment and the duration of the assessment.

Validation and Credibility

Because the ROC involves independent third-party validation, it carries more weight and credibility than a self-attested AOC. Acquiring banks, payment processors, and business partners often place greater confidence in ROC validation, particularly for high-risk or high-volume merchants.

Frequency and Timing

Both documents require annual renewal, but the ROC process is considerably more time-intensive. Organizations should typically begin ROC preparation three to six months before their compliance deadline, while an AOC can often be completed in a matter of weeks once the organization has achieved compliance with the applicable SAQ requirements.

Level of Technical Detail

The AOC focuses on confirming that specific requirements have been met, with yes/no responses and minimal supporting detail. The ROC provides extensive technical documentation, including testing methodologies, evidence collection procedures, sample sizes, and detailed findings for each requirement and sub-requirement.

Importance of AOC and ROC in Compliance

Both the AOC and ROC serve critical functions in the payment security ecosystem, and understanding their importance helps organizations prioritize compliance efforts appropriately.

Maintaining Merchant Account Status

Your acquiring bank or payment processor requires proof of PCI DSS compliance to maintain your merchant account in good standing. Failure to provide the appropriate compliance documentation whether an AOC or ROC can result in increased transaction fees, monthly non-compliance penalties, or even termination of your ability to accept credit card payments. For many businesses, losing the ability to process cards would be financially catastrophic.

Protecting Customer Data and Trust

Beyond regulatory requirements, these compliance documents represent your organization's commitment to protecting customer payment information. In an era where data breaches regularly make headlines and erode consumer confidence, demonstrating PCI DSS compliance through proper AOC or ROC documentation shows customers that you take their security seriously. This commitment can differentiate your business in competitive markets and build long-term customer loyalty.

Mitigating Legal and Financial Liability

In the unfortunate event of a data breach, having current and accurate compliance documentation can help mitigate legal exposure and financial penalties. While PCI DSS compliance doesn't guarantee immunity from breaches, it demonstrates due diligence in implementing industry-standard security controls. Conversely, lacking proper compliance documentation can result in severe consequences, including fines from card brands ranging from $5,000 to $100,000 per month, forensic investigation costs, card reissuance fees, and potential civil liability.

Facilitating Business Relationships

Many organizations, particularly in B2B environments, require vendors and partners to demonstrate PCI DSS compliance before entering into business relationships. Having a current AOC or ROC ready to present can accelerate contract negotiations, open doors to new business opportunities, and satisfy procurement requirements for security-conscious clients.

Establishing Security Baseline and Best Practices

The process of completing an SAQ for an AOC or undergoing a QSA assessment for a ROC forces organizations to examine their security posture comprehensively. This scrutiny helps identify vulnerabilities, establish security baselines, and implement industry best practices that extend beyond payment card security to benefit overall information security programs.

Supporting Cyber Insurance Requirements

Many cyber insurance policies now require evidence of PCI DSS compliance as a condition of coverage or to maintain favorable premium rates. Your AOC or ROC serves as the documentation needed to satisfy these insurance requirements and potentially reduce coverage costs.

Enabling Continuous Compliance Culture

The annual requirement to produce an AOC or ROC encourages organizations to maintain ongoing compliance efforts rather than treating security as a one-time checkbox exercise. This regular validation cycle promotes a culture of continuous security improvement and helps ensure that compliance doesn't degrade between assessment periods.

Updates in PCI DSS Compliance Affecting AOC and ROC

The PCI Security Standards Council regularly updates the PCI DSS framework to address evolving security threats and technological changes. Understanding recent updates is crucial for organizations preparing their AOC or ROC documentation.

PCI DSS Version 4.0 Transition

The most significant recent change is the release of PCI DSS version 4.0 in March 2022, with updated SAQs and ROC reporting templates released subsequently. While version 3.2.1 remained valid through March 31, 2024, all organizations must now comply with version 4.0 requirements. This transition impacts both AOC and ROC documentation significantly.

Customized Implementation Approach

PCI DSS 4.0 introduces a new concept called "customized implementation," which allows organizations to implement security controls in alternative ways, provided they meet the same security objectives as the defined requirements. This flexibility must be thoroughly documented in ROC reports, with QSAs validating that customized approaches achieve equivalent or greater security than traditional implementations.

Enhanced Flexibility and Risk-Based Requirements

Version 4.0 designates certain requirements as "defined approach requirements" (mandatory for all organizations) and others as "customized approach requirements" (allowing alternative implementations). This distinction affects how compliance is documented in both AOC and ROC formats, requiring clearer specification of which approach an organization follows for each requirement.

Expanded Scope Definitions

The updated standard provides clearer guidance on scoping the cardholder data environment, which directly impacts the complexity and depth of ROC assessments. Organizations must now document their scoping process more thoroughly, including how they segment networks, identify all system components, and justify exclusions from the assessment scope.

New and Evolved Requirements

PCI DSS 4.0 introduces several new requirements and modifies existing ones, all of which must be addressed in compliance documentation. Key additions include enhanced multi-factor authentication requirements, targeted risk analysis for cryptographic protocols, and increased focus on detection and response capabilities. Both AOC and ROC documents must reflect compliance with these updated requirements.

Targeted Risk Analysis Expectations

Version 4.0 places greater emphasis on risk-based approaches, requiring organizations to conduct targeted risk analyses for certain requirements. These risk analyses must be documented appropriately in compliance reports, with ROC assessments requiring QSAs to validate the adequacy and completeness of risk assessment processes.

Service Provider Designations

The updated standard refines how service providers are classified and their corresponding compliance obligations. This affects both the AOC requirements for service providers completing SAQs and the ROC requirements for those undergoing QSA assessments, with clearer delineation of responsibilities in multi-party payment environments.

Validation Documentation Requirements

PCI DSS 4.0 specifies more stringent documentation requirements for demonstrating ongoing compliance. Organizations must maintain more comprehensive evidence of security control implementation and effectiveness, which impacts what documentation must be collected and presented during both self-assessment and QSA validation processes.

Organizations should work closely with their QSA or compliance advisors to understand how these changes specifically affect their compliance documentation requirements and begin addressing any gaps well before their annual validation deadline.

Frequently Asked Questions (FAQs)

Q: How long is an AOC or ROC valid?

A: Both documents are typically valid for one year from the date of validation. Organizations must complete a new assessment and obtain updated documentation annually to maintain continuous compliance. Some acquiring banks may require validation more frequently for high-risk merchants.

Q: Can a small business ever need a ROC instead of an AOC?

A: Yes, in certain circumstances. While transaction volume is the primary determinant, some acquiring banks or payment processors may require smaller merchants to obtain a ROC due to specific risk factors, previous compliance issues, or the nature of their business. Always check with your acquiring bank for specific requirements.

Q: What happens if I can't complete all requirements for my AOC?

A: If your self-assessment reveals non-compliance with certain requirements, you should not submit an incomplete or inaccurate AOC. Instead, develop a remediation plan to address gaps, implement necessary controls, and then complete the assessment honestly. Submitting false compliance information can result in significant penalties and loss of merchant privileges.

Q: Do I need both an AOC and a ROC?

A: No, you typically need one or the other, depending on your merchant level and transaction volume. Large merchants requiring a ROC will receive an AOC as part of the ROC package from their QSA, but smaller merchants completing SAQs only need to submit their AOC.

Q: How much does a QSA assessment for a ROC typically cost?

A: Costs vary widely based on your environment's complexity, the number of locations, transaction types, and existing security posture. Small to mid-sized organizations might expect to pay $15,000 to $50,000, while large enterprises with complex environments can pay $100,000 or more for a comprehensive ROC assessment.

Q: What's the difference between PCI DSS compliance and PA-DSS?

A: PCI DSS (Payment Card Industry Data Security Standard) applies to merchants and service providers that store, process, or transmit cardholder data. PA-DSS (Payment Application Data Security Standard) was a separate standard for software vendors selling payment applications. PA-DSS was retired in October 2022 and replaced by the Software Security Framework within PCI DSS.

Q: Can I switch from ROC to AOC if my transaction volume decreases?

A: Yes, if your annual transaction volume drops below the Level 1 threshold and remains there consistently, you may be able to transition to SAQ validation with an AOC instead of continuing with annual ROC assessments. However, you should confirm this change with your acquiring bank, as they may have specific requirements for making this transition.

Q: Who should sign the AOC for my organization?

A: The AOC should be signed by an authorized representative who has the authority to attest to compliance on behalf of your organization. This is typically an executive-level individual such as a CEO, CFO, CIO, or CISO who understands the compliance status and accepts responsibility for the attestation's accuracy.

Conclusion

Understanding the difference between AOC and ROC is fundamental to navigating the PCI DSS compliance landscape effectively. While the AOC represents a self-attested declaration of compliance suitable for smaller merchants with less complex environments, the ROC provides independent third-party validation required for larger organizations processing significant transaction volumes. Both documents serve the critical purpose of demonstrating commitment to payment security, protecting customer data, and maintaining the trust necessary to participate in the payment card ecosystem.

The importance of these compliance documents extends far beyond simply satisfying acquiring bank requirements. They represent your organization's security posture, influence customer confidence, impact business relationships, and can significantly affect your bottom line through reduced breach risk and associated costs. With the evolution to PCI DSS version 4.0 bringing more nuanced requirements and greater flexibility, staying current with compliance documentation has become both more complex and more important than ever.

If you're completing your first SAQ and AOC or preparing for your tenth annual ROC assessment, approaching compliance as an ongoing commitment rather than an annual checkbox exercise will serve your organization well. The investment in proper compliance documentation pays dividends in enhanced security, reduced risk, and the peace of mind that comes from knowing your customers' payment information is protected according to industry-leading standards.

Contact Regulance today to schedule a compliance consultation and discover how we can transform your PCI DSS compliance from a burden into a competitive advantage. Your customers trust you with their payment information. Let Regulance help you prove you're worthy of that trust.