8 PCI DSS Compliance Tips to Protect Your Business

Introduction

PCI DSS (Payment Card Industry Data Security Standard) sets the security bar for organizations that handle payment cards. Beyond avoiding fines and fines from card brands, meeting PCI DSS reduces fraud risk, protects customer trust, and lowers the operational headaches that come with data breaches. The good news: compliance is achievable with the right controls, clear ownership, and a bit of discipline.

This guide breaks down what PCI DSS is, gives you 8 practical, implementable compliance tips, answers common FAQs, and finishes with a clear takeaway to help you take action on compliance.

A brief summary about PCI DSS

PCI DSS is a set of security requirements created by major card brands (Visa, MasterCard, American Express, Discover, JCB) to protect cardholder data. The standard covers areas like network security, access controls, encryption, monitoring, and policy-driven processes. There are 12 core requirements grouped into domains (build and maintain secure networks, protect cardholder data, manage vulnerabilities, etc.). Your exact obligations depend on your merchant level and how payment data flows through your systems.

All merchants that accept payment cards must meet PCI DSS requirements, but the specific obligations depend on your annual transaction volume and breach history:

- Level 1: More than 6 million transactions per year (online + in-person), or any merchant that has experienced a data breach. Level 1 merchants face the strictest rules: annual third-party audits (ROC), continuous network scans, and yearly compliance reporting.

- Level 2: 1 million – 6 million transactions per year. These merchants typically require formal assessments and periodic scans, but not always a full ROC unless requested.

- Level 3: 20,000 – 1 million online transactions per year. Level 3 merchants generally complete a Self-Assessment Questionnaire (SAQ) and follow quarterly ASV scans.

- Level 4: Fewer than 20,000 online transactions per year, or up to 1 million regular (in-person) transactions. Level 4 merchants most commonly validate via SAQ and quarterly ASV scans; scope and exact requirements can vary by acquirer.

Your merchant level determines your compliance requirements under PCI DSS - smaller merchants (level 4) can submit self-assessments and complete a quarterly scan with an Approved Scanning Vendor (ASV). In contrast, level 1 merchants are subject to more in-depth compliance requirements, including annual third-party audits, network scans, and annual compliance reports.

8 PCI DSS Compliance Tips

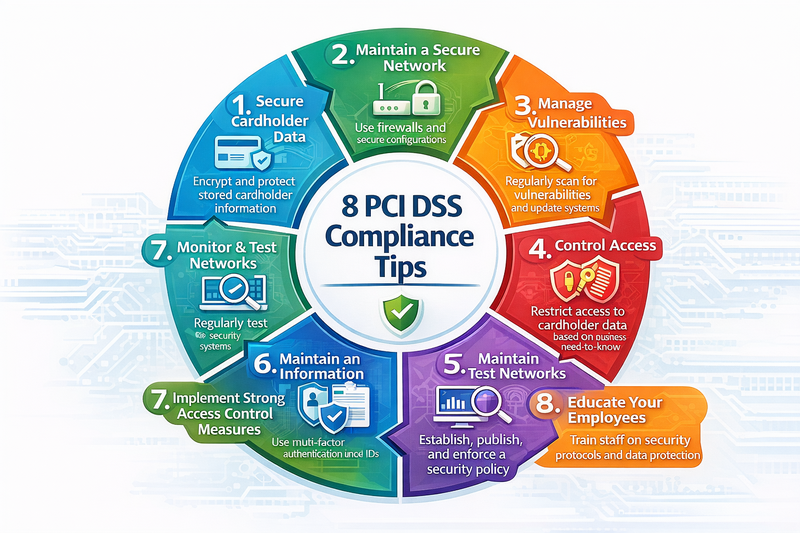

1. Map cardholder data flows precisely

Start by documenting exactly where card data is collected, stored, processed, and transmitted. A clear data-flow map makes scope reduction possible and reveals systems that must be hardened or segmented.

Action: Draw a simple diagram and list every system, API, third party, and person that touches card data.

2. Reduce scope with tokenization & PCI-approved processors

The less card data you touch, the easier compliance becomes. Offload storage and processing to a PCI-compliant payment gateway or use tokenization so your systems never store raw card numbers.

Action: Move payment capture to hosted fields or redirect pages from a PCI-compliant provider.

3. Segment networks and apply strict ACLs

Isolate payment environments from the rest of your network using segmentation and firewalls. Limiting access reduces attack surface and often lowers audit scope.

Action: Ensure only necessary systems can reach your payment servers; log and review firewall rules.

4. Enforce strong access controls and MFA

Limit card-data access on a need-to-know basis. Use role-based access, unique user IDs, and require multi-factor authentication (MFA) for admin and remote access. Remove stale accounts promptly.

Action: Audit user accounts quarterly and enable MFA for all privileged access.

5. Encrypt cardholder data in transit and at rest

Use modern TLS for data in transit and strong encryption for any stored data. Manage encryption keys securely (separate from encrypted data).

Action: Verify TLS configurations (no deprecated ciphers) and implement key rotation policies.

6. Log, monitor, and retain security event data

Capture logs from firewalls, servers, authentication systems, and payment systems. Monitor for anomalies, maintain log retention as required by your level, and test your alerting.

Action: Set up central logging and at least one alert for suspicious activity (e.g., repeated failed logins).

7. Patch and manage vulnerabilities regularly

Keep systems and third-party software patched. Run scheduled vulnerability scans and remediate findings quickly. For external-facing assets, run quarterly scans from an Approved Scanning Vendor (ASV) if required.

Action: Create a prioritized remediation backlog and track mean time to patch.

8. Document policies and train your team

PCI DSS relies on people and processes as much as tech. Maintain written policies for acceptable use, incident response, and change control. Train staff on phishing, data handling, and reporting procedures.

Action: Run brief quarterly training and test staff with a phishing simulation.

FAQs

Q: Do I need PCI DSS if I use Stripe/PayPal?

A: If you never touch card data (use hosted payment pages or client-side tokenization), your scope is dramatically reduced, but you still must validate your approach (usually a SAQ) and ensure your provider is PCI-compliant.

Q: What’s the difference between SAQ and ROC?

A: SAQ (Self-Assessment Questionnaire) is for smaller merchants who self-validate compliance. A ROC (Report on Compliance) is produced by a Qualified Security Assessor (QSA) for larger or more complex entities.

Q: How often must I be assessed?

A: Many merchants complete annual assessments. Additionally, vulnerability scans or external scans might be required quarterly depending on your merchant level.

Q: Will PCI DSS make me immune to breaches?

A: No standard guarantees immunity. PCI DSS reduces risk significantly but must be paired with good security hygiene, active monitoring, and incident readiness.

Q: What’s the fastest way to reduce PCI scope?

A: Move to a hosted payment solution or tokenization so card data never touches your servers. This is often the quickest and most cost-effective scope-reduction approach.

Conclusion

PCI DSS compliance is a practical, business-critical process, not an insurmountable IT project. By mapping your cardholder data flows, reducing scope using tokenization, enforcing strong access controls, encrypting data, monitoring logs, patching vulnerabilities, and training staff, you’ll both satisfy card brand requirements and protect your customers. Start with the highest-impact items: scope reduction and access controls. Then treat compliance as an ongoing program, not a one-time checklist.

Your next PCI DSS audit doesn’t have to be stressful; See how Regulance Ai makes compliance simple and effective.